As we like to say here at Triple Whale, you are not your ROAS, or return on ad spend. But if you really want to dig into an ad spend metric that will propel your growth, you should probably know a critical derivative of your ROAS called breakeven ROAS. Here, dig into why this metric is so important, how to calculate it, and what it means in the context of other measurements of your success.

ROAS, or return on ad spend, is a measure of the effectiveness of a specific ad campaign. You calculate it by dividing your ad revenue by your ad spend. This tells you how much revenue you’re making on a specific campaign for every dollar your business spent on that campaign.

It’s different from your return on investment. When comparing ROI vs. ROAS, remember that ROI measures the profit you made from everything you’ve invested in your business, not just what you’ve made from and invested in a specific ad campaign.

And while that’s a relatively straightforward calculation, there are many derivatives of ROAS that complicate things a bit, like in-platform ROAS, blended ROAS, target ROAS, Facebook ROAS, breakeven ROAS, and more.

So what does breakeven ROAS mean, exactly? Your BEROAS is a calculation of when you break even on acquiring a customer. You’re not making money on an ad campaign (which ideally you want and would constitute a “good” ROAS), but you’re not losing money, either—you’re breaking even.

This metric depends on three components, also known as your unit economics:

These unit economics are used together in the breakeven ROAS formula below, essentially like a profit-and-loss (P&L) statement at the level of a new customer’s first order.

Why does that matter? If you’re a high-growth business, your current top-priority objective may be to acquire as many new customers as possible, as quickly as possible, rather than making money on acquiring new customers.

When that’s the case, your business may take a loss up front in order to acquire those new customers. The hope is they will eventually become return customers. If you can break even on their first purchase, every purchase thereafter will generate a positive contribution margin on a customer-level basis.

Keep in mind this strategy is more fruitful if your offerings inspire repeat purchases. It’s less effective if your product is a one-and-done type purchase.

Once you build a critical mass of customers, the profit you make on returning customers is entirely gross profit, which may even be high enough to cover expenses like salaries, rent, travel, and more, keeping your business profitable.

Many brands of the early 2010s got themselves into trouble by dipping so far into the red on contribution margin on the first purchase. Even with strong customer lifetime values (CLV), they never were able to generate enough recurring revenue to cover the cost of acquisition. This is sure to hurt any business once it's unable to raise capital in an effort to outrun operational inefficiencies.

Today, brands are looking to generate positive cash flow sooner than later, and starting at zero means even $1 of subsequent cash flow can get your unit economics into the black.

Now that you understand why breaking even is more of a leg up than it sounds, you’re ready to calculate breakeven ROAS.

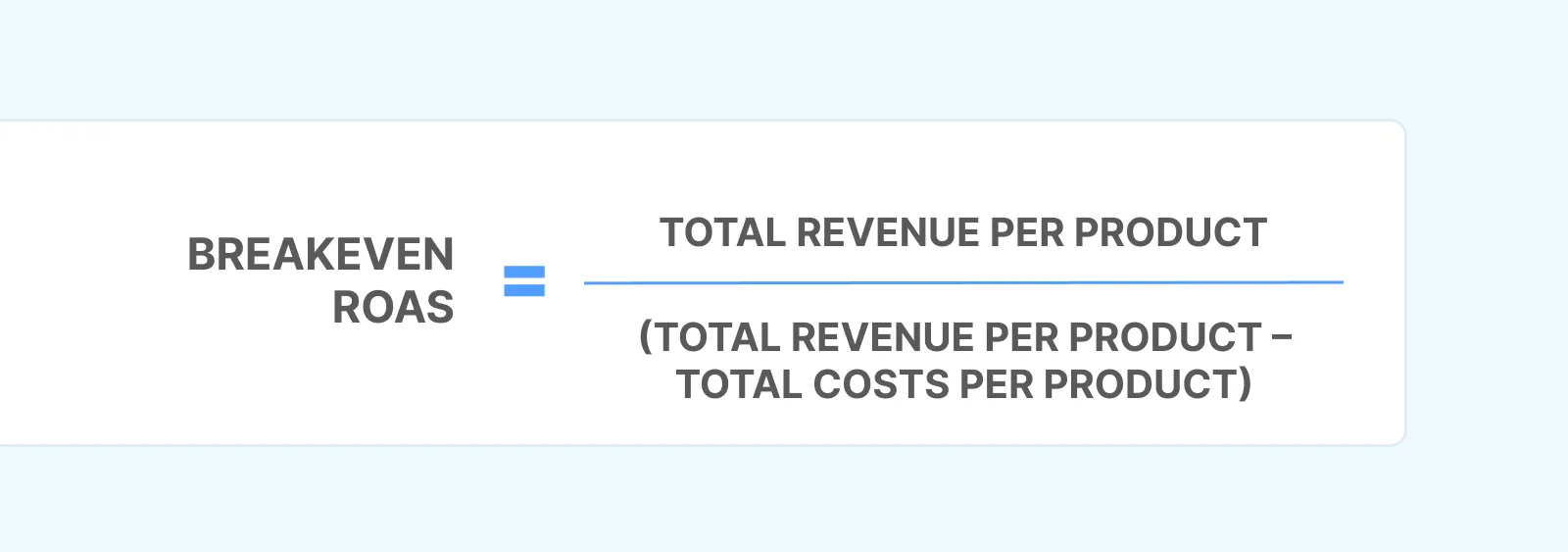

To do so, multiply your AOV by your gross margin. Then, subtract your CAC. When the result you get is zero, your AOV divided by your CAC equals your breakeven ROAS.

In other words, the equation for how to calculate breakeven ROAS looks like this:

If: AOV x gross margin - CAC = 0

Then: AOV/CAC = BEROAS

As a quick refresher, that’s a little different from the typical ROAS formula, which is calculated by dividing your ad revenue by the cost of those ads.

You can also approach your BEROAS calculation a little differently:

Simpler still is using our breakeven ROAS calculator, which can do the math for you.

Let’s see how that plays out in a real-world scenario.

Imagine your ecommerce store has an AOV of $50 and a gross margin of 50%. That means your gross profit is $25.

If you have a CAC of $25, your net income is exactly zero dollars. That would make your breakeven ROAS $50 divided by $25, or 2, meaning $2 for every dollar spent is the minimum ROAS your campaigns need to have in order to achieve marketing efficiency.

Here’s what those formulas look like for this example:

($50 x 0.5) - $25 = 0

50/25 = 2

Your breakeven ROAS is an important data point, but it, like so many other marketing metrics, offers you even more insights when used in the context of other information.

That’s because breakeven ROAS doesn’t capture all of your costs, such as salaries, legal fees, banking fees, taxes, interest, and more.

We call these expenses general and administrative expenses, or G&A. Breakeven ROAS simply doesn’t take these costs into account, but you still need to be aware of your fixed overhead. It’s too simplistic to believe that as long as you’re breaking even on a first purchase that your business is going to make it. There are many other factors that go into generating net income profitability.

It’s also worthwhile to consider your BEROAS alongside your CLV, because it can help you understand the long-term value of your advertising efforts at a higher level than simply breaking even. Keeping these metrics in mind together will help you establish more accurate targets for profitability and find the balance between acquiring new customers and retaining your loyal base.

A breakeven ROAS is just one of the many derivatives of ROAS that exist. It can help set you up for healthy unit economics, balance your growth with your runway, and much more, when harnessed correctly. But for long-lasting success, you need to understand the various ways in which your advertising generates return. Triple Whale can help you convert visitors, retain customers, and improve ROAS — book a demo today!

As we like to say here at Triple Whale, you are not your ROAS, or return on ad spend. But if you really want to dig into an ad spend metric that will propel your growth, you should probably know a critical derivative of your ROAS called breakeven ROAS. Here, dig into why this metric is so important, how to calculate it, and what it means in the context of other measurements of your success.

ROAS, or return on ad spend, is a measure of the effectiveness of a specific ad campaign. You calculate it by dividing your ad revenue by your ad spend. This tells you how much revenue you’re making on a specific campaign for every dollar your business spent on that campaign.

It’s different from your return on investment. When comparing ROI vs. ROAS, remember that ROI measures the profit you made from everything you’ve invested in your business, not just what you’ve made from and invested in a specific ad campaign.

And while that’s a relatively straightforward calculation, there are many derivatives of ROAS that complicate things a bit, like in-platform ROAS, blended ROAS, target ROAS, Facebook ROAS, breakeven ROAS, and more.

So what does breakeven ROAS mean, exactly? Your BEROAS is a calculation of when you break even on acquiring a customer. You’re not making money on an ad campaign (which ideally you want and would constitute a “good” ROAS), but you’re not losing money, either—you’re breaking even.

This metric depends on three components, also known as your unit economics:

These unit economics are used together in the breakeven ROAS formula below, essentially like a profit-and-loss (P&L) statement at the level of a new customer’s first order.

Why does that matter? If you’re a high-growth business, your current top-priority objective may be to acquire as many new customers as possible, as quickly as possible, rather than making money on acquiring new customers.

When that’s the case, your business may take a loss up front in order to acquire those new customers. The hope is they will eventually become return customers. If you can break even on their first purchase, every purchase thereafter will generate a positive contribution margin on a customer-level basis.

Keep in mind this strategy is more fruitful if your offerings inspire repeat purchases. It’s less effective if your product is a one-and-done type purchase.

Once you build a critical mass of customers, the profit you make on returning customers is entirely gross profit, which may even be high enough to cover expenses like salaries, rent, travel, and more, keeping your business profitable.

Many brands of the early 2010s got themselves into trouble by dipping so far into the red on contribution margin on the first purchase. Even with strong customer lifetime values (CLV), they never were able to generate enough recurring revenue to cover the cost of acquisition. This is sure to hurt any business once it's unable to raise capital in an effort to outrun operational inefficiencies.

Today, brands are looking to generate positive cash flow sooner than later, and starting at zero means even $1 of subsequent cash flow can get your unit economics into the black.

Now that you understand why breaking even is more of a leg up than it sounds, you’re ready to calculate breakeven ROAS.

To do so, multiply your AOV by your gross margin. Then, subtract your CAC. When the result you get is zero, your AOV divided by your CAC equals your breakeven ROAS.

In other words, the equation for how to calculate breakeven ROAS looks like this:

If: AOV x gross margin - CAC = 0

Then: AOV/CAC = BEROAS

As a quick refresher, that’s a little different from the typical ROAS formula, which is calculated by dividing your ad revenue by the cost of those ads.

You can also approach your BEROAS calculation a little differently:

Simpler still is using our breakeven ROAS calculator, which can do the math for you.

Let’s see how that plays out in a real-world scenario.

Imagine your ecommerce store has an AOV of $50 and a gross margin of 50%. That means your gross profit is $25.

If you have a CAC of $25, your net income is exactly zero dollars. That would make your breakeven ROAS $50 divided by $25, or 2, meaning $2 for every dollar spent is the minimum ROAS your campaigns need to have in order to achieve marketing efficiency.

Here’s what those formulas look like for this example:

($50 x 0.5) - $25 = 0

50/25 = 2

Your breakeven ROAS is an important data point, but it, like so many other marketing metrics, offers you even more insights when used in the context of other information.

That’s because breakeven ROAS doesn’t capture all of your costs, such as salaries, legal fees, banking fees, taxes, interest, and more.

We call these expenses general and administrative expenses, or G&A. Breakeven ROAS simply doesn’t take these costs into account, but you still need to be aware of your fixed overhead. It’s too simplistic to believe that as long as you’re breaking even on a first purchase that your business is going to make it. There are many other factors that go into generating net income profitability.

It’s also worthwhile to consider your BEROAS alongside your CLV, because it can help you understand the long-term value of your advertising efforts at a higher level than simply breaking even. Keeping these metrics in mind together will help you establish more accurate targets for profitability and find the balance between acquiring new customers and retaining your loyal base.

A breakeven ROAS is just one of the many derivatives of ROAS that exist. It can help set you up for healthy unit economics, balance your growth with your runway, and much more, when harnessed correctly. But for long-lasting success, you need to understand the various ways in which your advertising generates return. Triple Whale can help you convert visitors, retain customers, and improve ROAS — book a demo today!

.webp)

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)