A cash conversion cycle (CCC) is the amount of time it takes a business to convert its investments in inventory and other resources into cash from sales. A negative CCC occurs when the cash inflows of customer payments are greater than or equal to the outflow required to purchase inventory and other resources, resulting in a negative conversion cycle. In other words, when customers pay for the items before the business pays the supplier for the inventory, a negative CCC is created.

The importance of understanding and attaining a negative cash conversion cycle cannot be overstated. Many of the mega retail companies boast a negative cash conversion cycle, however, it may be tricky for small businesses to reach this state.

The goal of this article is to provide an understanding of the negative cash conversion cycle, its calculation, and what it means in terms of business performance. We will also discuss some common causes of a negative CCC so you can optimize them to achieve a NCCC.

The first step towards managing NCCC is calculating it accurately.

First, you have to understand the business period that you want to measure (usually a month or quarter). Many experts recommend 14 weeks or one quarter.

After which, you have to gather information on your accounting. These include:

Once these values are obtained, you can calculate the following factors needed to calculate the CCC:

DIO is the average number of days it takes a business to turn its inventory into sales.

It is calculated by dividing the average inventory level (beginning inventory + ending inventory/2) by the cost of goods sold (COGS) and then multiplying it by the number of days in the period (usually 365).

DIO = ((Beginning Inventory Value + Ending Inventory Value)/(COGS/2)) * Period

DSO is the average number of days it takes a business to collect payments from its customers.

DSO is calculated by dividing accounts receivable by the net sales (revenue – COGS) and then multiplying it by the number of days in the period.

DIO = ((Beginning Inventory Value + Ending Inventory Value)/(COGS/2)) * Period

DPO is the average number of days it takes a business to pay its suppliers. Similar to the above, this calculation looks at your accounts payable turnover.

It is calculated by dividing the accounts payable at the beginning of the period by total purchases (COGS + any other purchases) and then multiplying it by the number of days in the period.

DPO = ((Beginning Accounts Payable + Ending Accounts Payable)/COGS *2))* Period

Once all the individual factors are calculated, you can then calculate your Cash Conversion Cycle. The formula is:

Cash Conversion Cycle (CCC) = DIO + DSO – DPO

For example, let's say you have the following values for a month:

Using these values, we can calculate DIO, DSO, and DPO as follows:

Therefore, the Cash Conversion Cycle (CCC) = 30 + 7.5 - 15 = 22.5 days

A negative CCC indicates that the business's vendors are financing their operations. Most businesses aim to have a low cash conversion cycle or negative cash conversion cycle. This is because it indicates that the business can generate more cash from its sales than what it spends on purchasing new inventory and paying its bills. This is a sign of good financial health, management, and profitability as the business can use its suppliers’ money to generate cash flow.

For example, large retailers such as Amazon often have negative CCCs as they can take advantage of the suppliers’ credit and turn their inventory quickly.

However, eCommerce businesses tend to have high CCCs as they do not have the luxury of relying on their supplier’s credit to finance their operations. They tend to reinvest the money generated from their operations into purchasing more inventory or expanding their operations, in hopes of generating more sales.

A negative cash conversion cycle can have a significant impact on business performance and cash flow. If the CCC is too high, it indicates that the business is not generating enough cash from its sales to cover the costs of new inventory purchases or payments to suppliers. This can lead to cash flow constraints, which can hamper the business’s ability to pay for its future inventories, operations, and growth.

On the other hand, if the CCC is too low, it indicates that the business is not taking full advantage of its suppliers’ credit. Businesses should aim to strike a balance between taking full advantage of their suppliers’ credit.

Various factors can lead to a negative cash conversion cycle. These include:

Inventory turnover is the number of times inventory is sold in a period. Businesses should aim for a higher or quicker inventory turnover, that is, they should sell their inventory as soon as possible, which translates into a decrease in their cash conversion cycle.

Businesses should ensure that they maintain an optimal inventory turnover rate by monitoring the demand for their products and regularly assessing their current inventory levels.

Accounts receivable turnover is the number of times a company can collect its receivables in a given period. The goal is to have a quicker accounts receivable turnover, which can be achieved by reducing the time it takes to invoice customers and receive payments.

Your accounts receivable turnover affects your cash conversion cycle. By reducing the time it takes to generate cash from your sales, you can attain a negative CCC.

Accounts payable turnover is the number of times a business pays its creditors in a given period. Businesses should aim to have higher accounts payable turnover, that is, they should pay their creditors as soon as possible.

By paying your creditors quickly while improving the time it takes to receive payments from customers, you can reduce your CCC.

The key to achieving a negative cash conversion cycle is to adopt strategies that are tailored to their specific needs, these include:

While there are several strategies to help achieve a negative cash conversion cycle, there are also some best practices that can help businesses maintain their CCC in the long run.

Businesses should regularly evaluate the financial strength of their suppliers to ensure that they can pay their bills on time. Businesses should also consider building relationships with multiple suppliers to reduce the impact of any one supplier’s financial problems.

As a company, it is important to have efficient invoicing and accounts receivable processes in place. You should also ensure that they are following up on late payments and negotiating payment plans with customers who are unable to pay the full amount up front.

Similarly, you should review their customer credit criteria to ensure that they are setting the right terms. By offering perks such as discounts for early payments, businesses can incentivize customers to pay their invoices promptly.

Your inventory management process should be designed to maximize the turnover of your inventory. You should consider implementing a demand forecasting system to better manage their inventories and ensure that they are stocking the right amount of items.

Monitoring cash conversion cycles is important because it allows businesses to identify areas where they can make improvements. As a business, you should regularly assess its CCC and make the necessary adjustments to sustainably improve its cash flow.

A good cash conversion cycle is one where the time it takes to receive payment from customers is shorter than the time it takes to pay suppliers. Ideally, a business should aim for a cash conversion cycle of 1 day as the shorter the better.

By implementing the strategies mentioned above, businesses can improve their cash conversion cycle and take advantage of the financial benefits that come with it. You should also make sure to assess your CCC regularly and adjust the necessary processes to ensure that it is improved sustainably.

The negative cash conversion cycle can have a major impact on a business’s cash flow. Businesses should put processes in place to identify and optimize the underlying causes of the negative cash conversion cycle.

Taking the time to identify and integrate the right strategies can help businesses shorten the CCC. By doing this, businesses can ensure that their cash flow remains healthy and that they are taking advantage of all available opportunities.

Looking for a place to view your revenue, fixed costs, advertising costs, gross profit and net profit all in one place? Check out the Income Statement board in Triple Whale for a clear, bird's-eye view of your business's financial health.

A cash conversion cycle (CCC) is the amount of time it takes a business to convert its investments in inventory and other resources into cash from sales. A negative CCC occurs when the cash inflows of customer payments are greater than or equal to the outflow required to purchase inventory and other resources, resulting in a negative conversion cycle. In other words, when customers pay for the items before the business pays the supplier for the inventory, a negative CCC is created.

The importance of understanding and attaining a negative cash conversion cycle cannot be overstated. Many of the mega retail companies boast a negative cash conversion cycle, however, it may be tricky for small businesses to reach this state.

The goal of this article is to provide an understanding of the negative cash conversion cycle, its calculation, and what it means in terms of business performance. We will also discuss some common causes of a negative CCC so you can optimize them to achieve a NCCC.

The first step towards managing NCCC is calculating it accurately.

First, you have to understand the business period that you want to measure (usually a month or quarter). Many experts recommend 14 weeks or one quarter.

After which, you have to gather information on your accounting. These include:

Once these values are obtained, you can calculate the following factors needed to calculate the CCC:

DIO is the average number of days it takes a business to turn its inventory into sales.

It is calculated by dividing the average inventory level (beginning inventory + ending inventory/2) by the cost of goods sold (COGS) and then multiplying it by the number of days in the period (usually 365).

DIO = ((Beginning Inventory Value + Ending Inventory Value)/(COGS/2)) * Period

DSO is the average number of days it takes a business to collect payments from its customers.

DSO is calculated by dividing accounts receivable by the net sales (revenue – COGS) and then multiplying it by the number of days in the period.

DIO = ((Beginning Inventory Value + Ending Inventory Value)/(COGS/2)) * Period

DPO is the average number of days it takes a business to pay its suppliers. Similar to the above, this calculation looks at your accounts payable turnover.

It is calculated by dividing the accounts payable at the beginning of the period by total purchases (COGS + any other purchases) and then multiplying it by the number of days in the period.

DPO = ((Beginning Accounts Payable + Ending Accounts Payable)/COGS *2))* Period

Once all the individual factors are calculated, you can then calculate your Cash Conversion Cycle. The formula is:

Cash Conversion Cycle (CCC) = DIO + DSO – DPO

For example, let's say you have the following values for a month:

Using these values, we can calculate DIO, DSO, and DPO as follows:

Therefore, the Cash Conversion Cycle (CCC) = 30 + 7.5 - 15 = 22.5 days

A negative CCC indicates that the business's vendors are financing their operations. Most businesses aim to have a low cash conversion cycle or negative cash conversion cycle. This is because it indicates that the business can generate more cash from its sales than what it spends on purchasing new inventory and paying its bills. This is a sign of good financial health, management, and profitability as the business can use its suppliers’ money to generate cash flow.

For example, large retailers such as Amazon often have negative CCCs as they can take advantage of the suppliers’ credit and turn their inventory quickly.

However, eCommerce businesses tend to have high CCCs as they do not have the luxury of relying on their supplier’s credit to finance their operations. They tend to reinvest the money generated from their operations into purchasing more inventory or expanding their operations, in hopes of generating more sales.

A negative cash conversion cycle can have a significant impact on business performance and cash flow. If the CCC is too high, it indicates that the business is not generating enough cash from its sales to cover the costs of new inventory purchases or payments to suppliers. This can lead to cash flow constraints, which can hamper the business’s ability to pay for its future inventories, operations, and growth.

On the other hand, if the CCC is too low, it indicates that the business is not taking full advantage of its suppliers’ credit. Businesses should aim to strike a balance between taking full advantage of their suppliers’ credit.

Various factors can lead to a negative cash conversion cycle. These include:

Inventory turnover is the number of times inventory is sold in a period. Businesses should aim for a higher or quicker inventory turnover, that is, they should sell their inventory as soon as possible, which translates into a decrease in their cash conversion cycle.

Businesses should ensure that they maintain an optimal inventory turnover rate by monitoring the demand for their products and regularly assessing their current inventory levels.

Accounts receivable turnover is the number of times a company can collect its receivables in a given period. The goal is to have a quicker accounts receivable turnover, which can be achieved by reducing the time it takes to invoice customers and receive payments.

Your accounts receivable turnover affects your cash conversion cycle. By reducing the time it takes to generate cash from your sales, you can attain a negative CCC.

Accounts payable turnover is the number of times a business pays its creditors in a given period. Businesses should aim to have higher accounts payable turnover, that is, they should pay their creditors as soon as possible.

By paying your creditors quickly while improving the time it takes to receive payments from customers, you can reduce your CCC.

The key to achieving a negative cash conversion cycle is to adopt strategies that are tailored to their specific needs, these include:

While there are several strategies to help achieve a negative cash conversion cycle, there are also some best practices that can help businesses maintain their CCC in the long run.

Businesses should regularly evaluate the financial strength of their suppliers to ensure that they can pay their bills on time. Businesses should also consider building relationships with multiple suppliers to reduce the impact of any one supplier’s financial problems.

As a company, it is important to have efficient invoicing and accounts receivable processes in place. You should also ensure that they are following up on late payments and negotiating payment plans with customers who are unable to pay the full amount up front.

Similarly, you should review their customer credit criteria to ensure that they are setting the right terms. By offering perks such as discounts for early payments, businesses can incentivize customers to pay their invoices promptly.

Your inventory management process should be designed to maximize the turnover of your inventory. You should consider implementing a demand forecasting system to better manage their inventories and ensure that they are stocking the right amount of items.

Monitoring cash conversion cycles is important because it allows businesses to identify areas where they can make improvements. As a business, you should regularly assess its CCC and make the necessary adjustments to sustainably improve its cash flow.

A good cash conversion cycle is one where the time it takes to receive payment from customers is shorter than the time it takes to pay suppliers. Ideally, a business should aim for a cash conversion cycle of 1 day as the shorter the better.

By implementing the strategies mentioned above, businesses can improve their cash conversion cycle and take advantage of the financial benefits that come with it. You should also make sure to assess your CCC regularly and adjust the necessary processes to ensure that it is improved sustainably.

The negative cash conversion cycle can have a major impact on a business’s cash flow. Businesses should put processes in place to identify and optimize the underlying causes of the negative cash conversion cycle.

Taking the time to identify and integrate the right strategies can help businesses shorten the CCC. By doing this, businesses can ensure that their cash flow remains healthy and that they are taking advantage of all available opportunities.

Looking for a place to view your revenue, fixed costs, advertising costs, gross profit and net profit all in one place? Check out the Income Statement board in Triple Whale for a clear, bird's-eye view of your business's financial health.

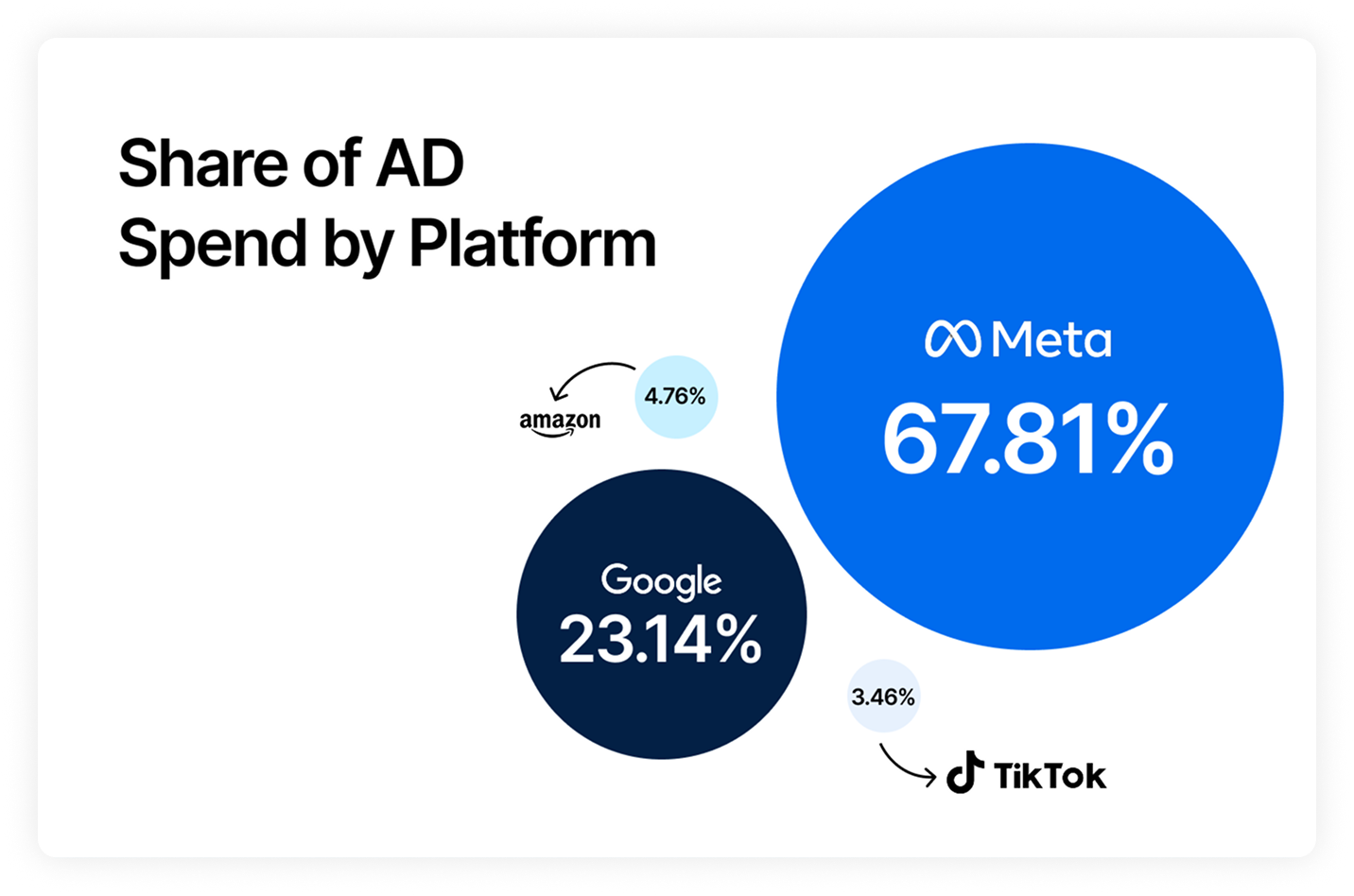

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)