The accounting for your e-commerce business differs from a traditional brick-and-mortar store in your hometown. With all of your transactions being electronic, there is an increased risk of error in your accounting records.

Three areas where e-commerce entrepreneurs commonly make mistakes are revenue recognition, inventory accounting, and sales tax compliance. Understanding common pitfalls can help your e-commerce business adapt and overcome them to produce accurate financial statements and tax remittances.

Revenue recognition is becoming more prevalent throughout the e-commerce realm with ASC 606 looking to streamline reporting. The money you receive in your bank account is not always the revenue that should be reported on the income statement. The first differentiation to make is earned versus deferred revenue.

Under ASC 606, revenue is not recognized until it is earned, which means all contractual obligations are satisfied. When a customer prepays for a contract, you will see cash hit your bank account, but the amounts will be deferred until your business satisfies your end of the contract.

In addition, many third-party payment processing apps take their fees directly off the top of your revenue. This means that the cash that hits your bank account understates revenue. For example, let’s say you earn $100 and have a $2 processing fee. The net amount that will be transferred to your bank account is $98. If your business only recorded the $98, revenue will be understated by $2.

This presents a risk to your business when the 1099-K reported to the IRS does not equal what your accounting records show. Additionally, if you go to sell your e-commerce business, many prospective buyers will look at the revenue your business is currently generating. Understating revenue will decrease your potential valuation and the amount you receive from the sale.

Improper inventory accounting is another common mistake that e-commerce businesses make. When your business purchases inventory, those amounts aren’t immediately deducted on the income statement. Instead, inventory sits on the balance sheet as a current asset until the item is sold. Only then can the amount be moved to the income statement under cost of goods sold.

This means that your inventory purchase orders aren’t deductible for tax purposes even though cash may have left your bank account. Counting on deducting the entire cost of inventory in that tax year leads to an unclear representation of your expected tax liability and can lead to underpaying estimates and foregoing the proper planning measures.

Closely managing inventory levels can help you understand when you need to reorder more, which items aren’t selling, and your breakeven cost. Even e-commerce businesses that engage in drop shipping need to have proper inventory accounting controls in place.

Purchasing too much inventory due to a lack of understanding of current levels can lead to cash flow issues. Making a purchase order when you have low funds in your business bank account isn’t ideal, especially if you have sufficient levels currently in inventory. Cash flow is a major issue for new and growing e-commerce businesses.

Like revenue recognition, sales tax compliance is on the rise with the recent supreme court case South Dakota v. Wayfair. This notable case creates the ability for states to impose sales tax on out-of-state purchases. Since e-commerce businesses have purchases across America, each state can collect sales tax from the revenue generated.

Many states do impose an economic nexus rule, meaning if your sales are under a certain threshold, you don’t have to file and pay taxes to that state. However, understanding when economic nexus is triggered can be confusing. Without the proper revenue tracking by state, your e-commerce business might miss paying sales tax in a certain state. This can result in back taxes with fines and penalties.

As an e-commerce business owner, you need to put the proper controls in place to track sales levels in each state. You can’t simply evaluate sales at the end of the year. Many states require monthly remittances, making it essential to check thresholds on a regular basis.

Running a successful e-commerce business relies on avoiding common mistakes made in the accounting function. Revenue recognition, inventory accounting, and sales tax compliance are three important areas to manage. You don’t want to report inaccurate tax returns or miss filing sales tax in a certain state because of lagging controls in your accounting function.

Sometimes working with an expert is what your e-commerce business needs to maximize accuracy. For more information or to talk to one of our team members, reach out today.

The accounting for your e-commerce business differs from a traditional brick-and-mortar store in your hometown. With all of your transactions being electronic, there is an increased risk of error in your accounting records.

Three areas where e-commerce entrepreneurs commonly make mistakes are revenue recognition, inventory accounting, and sales tax compliance. Understanding common pitfalls can help your e-commerce business adapt and overcome them to produce accurate financial statements and tax remittances.

Revenue recognition is becoming more prevalent throughout the e-commerce realm with ASC 606 looking to streamline reporting. The money you receive in your bank account is not always the revenue that should be reported on the income statement. The first differentiation to make is earned versus deferred revenue.

Under ASC 606, revenue is not recognized until it is earned, which means all contractual obligations are satisfied. When a customer prepays for a contract, you will see cash hit your bank account, but the amounts will be deferred until your business satisfies your end of the contract.

In addition, many third-party payment processing apps take their fees directly off the top of your revenue. This means that the cash that hits your bank account understates revenue. For example, let’s say you earn $100 and have a $2 processing fee. The net amount that will be transferred to your bank account is $98. If your business only recorded the $98, revenue will be understated by $2.

This presents a risk to your business when the 1099-K reported to the IRS does not equal what your accounting records show. Additionally, if you go to sell your e-commerce business, many prospective buyers will look at the revenue your business is currently generating. Understating revenue will decrease your potential valuation and the amount you receive from the sale.

Improper inventory accounting is another common mistake that e-commerce businesses make. When your business purchases inventory, those amounts aren’t immediately deducted on the income statement. Instead, inventory sits on the balance sheet as a current asset until the item is sold. Only then can the amount be moved to the income statement under cost of goods sold.

This means that your inventory purchase orders aren’t deductible for tax purposes even though cash may have left your bank account. Counting on deducting the entire cost of inventory in that tax year leads to an unclear representation of your expected tax liability and can lead to underpaying estimates and foregoing the proper planning measures.

Closely managing inventory levels can help you understand when you need to reorder more, which items aren’t selling, and your breakeven cost. Even e-commerce businesses that engage in drop shipping need to have proper inventory accounting controls in place.

Purchasing too much inventory due to a lack of understanding of current levels can lead to cash flow issues. Making a purchase order when you have low funds in your business bank account isn’t ideal, especially if you have sufficient levels currently in inventory. Cash flow is a major issue for new and growing e-commerce businesses.

Like revenue recognition, sales tax compliance is on the rise with the recent supreme court case South Dakota v. Wayfair. This notable case creates the ability for states to impose sales tax on out-of-state purchases. Since e-commerce businesses have purchases across America, each state can collect sales tax from the revenue generated.

Many states do impose an economic nexus rule, meaning if your sales are under a certain threshold, you don’t have to file and pay taxes to that state. However, understanding when economic nexus is triggered can be confusing. Without the proper revenue tracking by state, your e-commerce business might miss paying sales tax in a certain state. This can result in back taxes with fines and penalties.

As an e-commerce business owner, you need to put the proper controls in place to track sales levels in each state. You can’t simply evaluate sales at the end of the year. Many states require monthly remittances, making it essential to check thresholds on a regular basis.

Running a successful e-commerce business relies on avoiding common mistakes made in the accounting function. Revenue recognition, inventory accounting, and sales tax compliance are three important areas to manage. You don’t want to report inaccurate tax returns or miss filing sales tax in a certain state because of lagging controls in your accounting function.

Sometimes working with an expert is what your e-commerce business needs to maximize accuracy. For more information or to talk to one of our team members, reach out today.

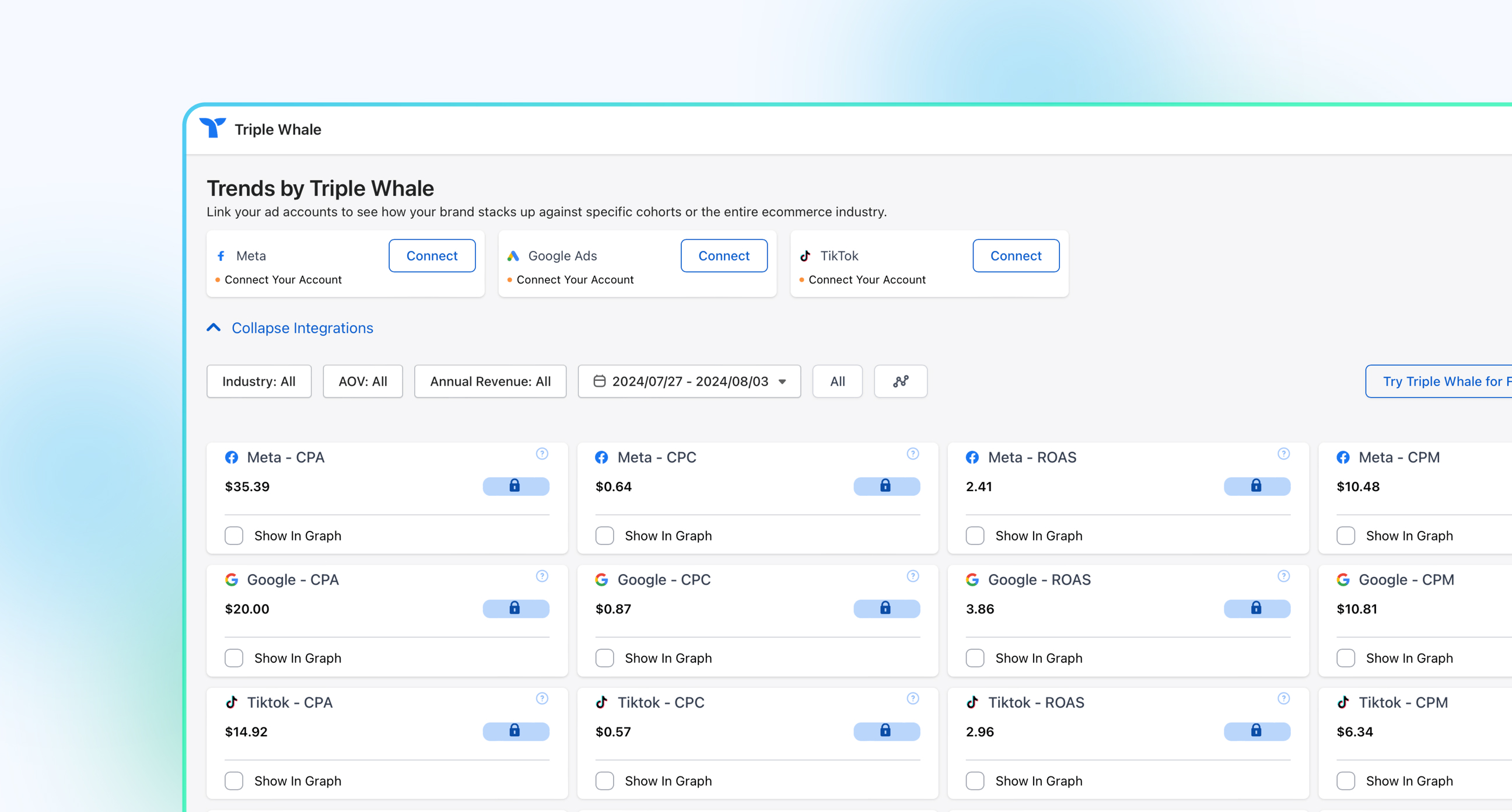

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)