Our benchmarks report will review common ad performance metrics for Google Ads across brands using Triple Whale to monitor and maximize their performance. This analysis includes over 18,000 brands for the period of January 1-December 31, 2025.

READ MORE | A Guide to Ecommerce Metrics

Additionally, we’ll break down the vertical-specific trends with data from the following industries:

The overall ad performance data for Google Ads in 2025 indicates a challenging ad platform marked by increased costs and declining efficiency. Marketing efficiency ratio (MER) improved by +9.86%, even as ROAS and conversion rate experienced drops (-10.03% and -9.28%, respectively).

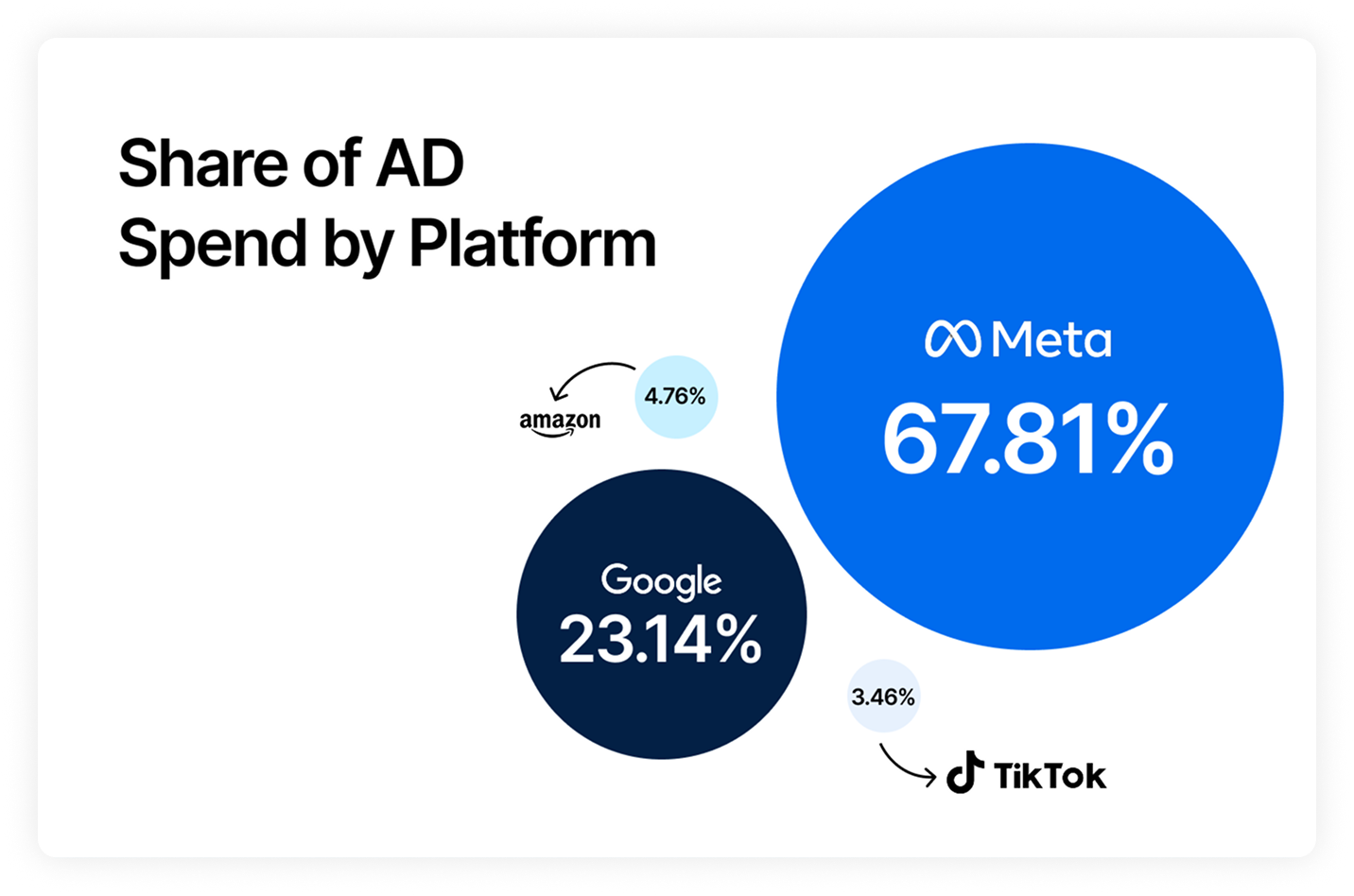

Triple Whale brands invested 23.03% of ad spend on Google Ads in 2025, second to only Meta (68.31%). While they’re the next big competitor to the Meta behemoth, the share of spend for Google Ads still dropped in 2025 by -9.67%.

Drops in efficiency metrics might explain why brands invested less heavily in Google Ads than the year prior. The median CPA rose by +12.35% to $23.74, and median CPM also jumped by +10.01% to $12.79.

Return on ad spend dropped by -10.03% to 3.68, and AOV essentially held steady with only a +0.57% increase. Although clickthrough rate (CTR) increased (+7.49%), conversion rate (CVR) dipped by -9.28%, meaning that customers were clicking on more ads, but converting less. This competitive environment means brands must optimize aggressively in order to maintain profitability.

CPA shows how much it costs to acquire a customer. In 2025, 13 of 14 industries showed increases in year-over-year growth. The sole exception was Pets & Animals, which achieved a -4.03% reduction in CPA to $25.15. Pets & Animals likely benefits from superior targeting optimization or stronger product-market fit compared to other verticals.

The most dramatic increases occurred in Travel Accessories & Luggage (+40.74% to $28.23) and Business Supplies & Equipment (+33.56% to $35.37). While not as staggering, the remaining industries all experiencing an increase in CPA points to increased competition driving up costs to acquire customers.

CPM increased universally across all industries in our dataset, with year-over-year growth ranging from +1.42% to +24.73%. Health & Wellness experienced the steepest CPM inflation at +24.73% to $19.69, followed by Automotive (+22.32% to $13.15). Even the smallest increase for Travel Accessories & Luggage (+1.42%) still represents the growing cost to reach audiences on Google Ads. Even though Apparel had the lowest overall CPM ($11.23), the +7.54% increase indicates even industries with relatively cheap CPMs are experiencing higher costs than years prior.

There was a decline in conversion rate for 13 of 14 industries in our dataset in 2025, representing a widespread erosion in customers actually converting on the ads they clicked. Only one industry improved their conversion rate, and it was Pets & Animals improving by +3.36% to 4.43%. The biggest declines in conversion rate were in Travel Accessories (-36.31% to 2.63%) and Business Supplies & Equipment (-18.48% to 2.70%).

In contrast to other metrics, CTR improved across all 14 industries in 2025, with growth ranging from +2.07% to +16.30%. Automotive led with +16.30% growth to 1.65% CTR, followed by Health & Wellness (+13.69% to 1.49%) and Home & Garden (+11.06% to 1.41%). A universal increase in CTR suggests these industries advertising on Google Ads have better ad creative quality and targeting precision across the board. However, a rising CTR combined with falling CVR indicates there might be a growing gap between ad promise and landing page delivery.

ROAS declined across 13 of 14 industries in 2025, mirroring the CVR pattern and confirming widespread efficiency deterioration. Only Pets & Animals improved ROAS, growing +2.51% to 2.84. The largest ROAS declines were in Travel Accessories & Luggage (-21.10% to 4.30), Health & Wellness (-15.64% to 2.12), and Consumer Electronics (-11.45% to 3.02).

AOV trends were the most variable across industries, with some showing growth and others declining. This suggests that category-specific dynamics are influencing these trends, rather than platform-wide pressure.

Business Supplies & Equipment led with a dramatic +31.65% increase to $113.25, while Consumer Electronics grew +16.70% to $120.95. The largest declines occurred in Travel Accessories & Luggage (-5.02% to $132.76) and Health & Wellness (-3.95% to $132.76).

MER increased across 12 of 14 industries in 2025, indicating advertisers are spending more on marketing relative to total revenue. The two exceptions were Pets & Animals (-1.95% to 0.33) and Business Supplies & Equipment (minimal +1.74% to 0.28). The largest MER increases occurred in Travel Accessories & Luggage (+22.51% to 0.21) and Health & Wellness (+14.12% to 0.40).

Google Ads performance in 2025 reflected a challenging environment for advertisers across nearly all industries, with increased cost per acquisition and declining ROAS. Overall, advertisers paid more for less efficient results.

These Google benchmarks provide a crucial reference for brands to optimize their ad strategies to ensure they maximize returns during the peak spending period upon us.

Get more free ecommerce benchmarks just like this! Check out Trends by Triple Whale.

Our benchmarks report will review common ad performance metrics for Google Ads across brands using Triple Whale to monitor and maximize their performance. This analysis includes over 18,000 brands for the period of January 1-December 31, 2025.

READ MORE | A Guide to Ecommerce Metrics

Additionally, we’ll break down the vertical-specific trends with data from the following industries:

The overall ad performance data for Google Ads in 2025 indicates a challenging ad platform marked by increased costs and declining efficiency. Marketing efficiency ratio (MER) improved by +9.86%, even as ROAS and conversion rate experienced drops (-10.03% and -9.28%, respectively).

Triple Whale brands invested 23.03% of ad spend on Google Ads in 2025, second to only Meta (68.31%). While they’re the next big competitor to the Meta behemoth, the share of spend for Google Ads still dropped in 2025 by -9.67%.

Drops in efficiency metrics might explain why brands invested less heavily in Google Ads than the year prior. The median CPA rose by +12.35% to $23.74, and median CPM also jumped by +10.01% to $12.79.

Return on ad spend dropped by -10.03% to 3.68, and AOV essentially held steady with only a +0.57% increase. Although clickthrough rate (CTR) increased (+7.49%), conversion rate (CVR) dipped by -9.28%, meaning that customers were clicking on more ads, but converting less. This competitive environment means brands must optimize aggressively in order to maintain profitability.

CPA shows how much it costs to acquire a customer. In 2025, 13 of 14 industries showed increases in year-over-year growth. The sole exception was Pets & Animals, which achieved a -4.03% reduction in CPA to $25.15. Pets & Animals likely benefits from superior targeting optimization or stronger product-market fit compared to other verticals.

The most dramatic increases occurred in Travel Accessories & Luggage (+40.74% to $28.23) and Business Supplies & Equipment (+33.56% to $35.37). While not as staggering, the remaining industries all experiencing an increase in CPA points to increased competition driving up costs to acquire customers.

CPM increased universally across all industries in our dataset, with year-over-year growth ranging from +1.42% to +24.73%. Health & Wellness experienced the steepest CPM inflation at +24.73% to $19.69, followed by Automotive (+22.32% to $13.15). Even the smallest increase for Travel Accessories & Luggage (+1.42%) still represents the growing cost to reach audiences on Google Ads. Even though Apparel had the lowest overall CPM ($11.23), the +7.54% increase indicates even industries with relatively cheap CPMs are experiencing higher costs than years prior.

There was a decline in conversion rate for 13 of 14 industries in our dataset in 2025, representing a widespread erosion in customers actually converting on the ads they clicked. Only one industry improved their conversion rate, and it was Pets & Animals improving by +3.36% to 4.43%. The biggest declines in conversion rate were in Travel Accessories (-36.31% to 2.63%) and Business Supplies & Equipment (-18.48% to 2.70%).

In contrast to other metrics, CTR improved across all 14 industries in 2025, with growth ranging from +2.07% to +16.30%. Automotive led with +16.30% growth to 1.65% CTR, followed by Health & Wellness (+13.69% to 1.49%) and Home & Garden (+11.06% to 1.41%). A universal increase in CTR suggests these industries advertising on Google Ads have better ad creative quality and targeting precision across the board. However, a rising CTR combined with falling CVR indicates there might be a growing gap between ad promise and landing page delivery.

ROAS declined across 13 of 14 industries in 2025, mirroring the CVR pattern and confirming widespread efficiency deterioration. Only Pets & Animals improved ROAS, growing +2.51% to 2.84. The largest ROAS declines were in Travel Accessories & Luggage (-21.10% to 4.30), Health & Wellness (-15.64% to 2.12), and Consumer Electronics (-11.45% to 3.02).

AOV trends were the most variable across industries, with some showing growth and others declining. This suggests that category-specific dynamics are influencing these trends, rather than platform-wide pressure.

Business Supplies & Equipment led with a dramatic +31.65% increase to $113.25, while Consumer Electronics grew +16.70% to $120.95. The largest declines occurred in Travel Accessories & Luggage (-5.02% to $132.76) and Health & Wellness (-3.95% to $132.76).

MER increased across 12 of 14 industries in 2025, indicating advertisers are spending more on marketing relative to total revenue. The two exceptions were Pets & Animals (-1.95% to 0.33) and Business Supplies & Equipment (minimal +1.74% to 0.28). The largest MER increases occurred in Travel Accessories & Luggage (+22.51% to 0.21) and Health & Wellness (+14.12% to 0.40).

Google Ads performance in 2025 reflected a challenging environment for advertisers across nearly all industries, with increased cost per acquisition and declining ROAS. Overall, advertisers paid more for less efficient results.

These Google benchmarks provide a crucial reference for brands to optimize their ad strategies to ensure they maximize returns during the peak spending period upon us.

Get more free ecommerce benchmarks just like this! Check out Trends by Triple Whale.

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)

.png)