Entrepreneurs have many options when it comes to financing their businesses. If you were going to put it into two buckets, you really have two choices: debt and equity.

What people often fail to realize is that the folks supplying the global debt markets are actually quite creative, and you have several vehicles to choose from. The reason there are so many different kinds is because every business is different, and there is so much money in these debt markets that market forces bring new products to life every day.

To help demystify the world of financing with debt, I want to touch on a handful of popular ecommerce debt instruments and explain a few reasons why each one may be right for your business.

I've broken these down as simply as I can -- and if you find this article valuable, let me know, and I can dig into more detail in a follow-up post.

Disclaimer: Debt can be a dangerous tool. This content is for informational purposes only.

The ABL is the old-school loan that is secured by your assets. In other words, the lender will give you money, and if you can't pay them back, they will take all of your stuff. Important to note: the amount of money they are willing to lend to you is a percentage of your assets, or what is called your ‘borrowing base.’

So let’s say you have $1MM of finished goods inventory in your warehouse. You could go to any of the ABL players and hopefully have them extend you a facility for around 50% of your asset value. Congratulations! You have a $500K asset backed debt facility to draw on.

In summary, ABL is usually a tough fit for startups growing very quickly and can be sneakily expensive. Additionally, secured loans can make for a pretty hairy outcome in a downside situation.

Venture debt is a bit more straightforward. Essentially, there exists a market of lenders who are willing to lend to you based on whether or not they think you will raise another equity round with a standard ‘Term Loan’.

A term loan is a classic principal + interest loan paid back over a specified duration of time. If you raise the next equity round, you can pay them back. If debt to equity capitalization is a spectrum of risk/reward, these lenders fall somewhere in the middle.

Fun fact: often you'll see funding announcements that are actually part equity, part venture debt. For instance, you might see a $20M Series B announcement. But behind the scenes, it was really $15M of Series B equity and $5M of venture debt. This helps the company get X more months of runway - without dilution - beyond the Series B issuance.

SBA loans are guaranteed by the government (via the Small Business Administration) and administered by banks for small businesses seeking capital. The most popular of these loans is known as the 7(a) loan program, which is a loan that has really flexible repayment terms as well as generally affordable interest rates.

Generally speaking, I would avoid these types of loans as a VC-backed founder as they come with personal guarantees (PGs), and if your business goes under, you are personally liable for the principal.

Pros:

Cons:

The MCA is my personal favorite for financing working capital of a hyper growth company. A merchant cash advance is a relatively new concept out of the last 5 years. Essentially, it is an open market receivables sale of your online business. What that means is you can sell your future revenue to any MCA supplier and they will advance you the amount of the receivables sale and charge you interest for putting the money in your pocket sooner.

MCA’s can get a bad rep, generally propagated by people who don’t fully understand them. It is true that these instruments can be ludicrously expensive when not negotiated properly. This is because they are paid back based on a remittance rate, or a percentage of your sales.

Therefore, if your sales begin to grow rapidly, you will pay back the loan + interest extremely quickly. If you end up paying off the whole loan +10% interest in 2 months because your business hit a huge growth spurt, you will have paid an effective 60% APR.

In my opinion, the reason this problem exists is because MCAs are so new that most lawyers don’t really understand them. Therefore, they are not able to effectively negotiate the terms of these deals, and unfortunately many founders end up paying ludicrous amounts in interest.

Good news: There is literally the easiest fix ever on this. You simply must negotiate remittance caps in order to achieve a desired APR. My last APR on an MCA was barely double digits, for a completely unsecured loan that I can draw on at any time. This is not always obvious to anyone who doesn't have familiarity modeling debt or IRRs, but it’s a fairly intuitive concept.

Pros:

Cons:

All in all, when it comes to financing, you have a lot of options to choose from -- especially on the debt side. It is important to understand all of the tools at your disposal so that you can ensure your business runs as smoothly as possible, properly finance operations, and avoid unnecessarily diluting your equity in the process.

Entrepreneurs have many options when it comes to financing their businesses. If you were going to put it into two buckets, you really have two choices: debt and equity.

What people often fail to realize is that the folks supplying the global debt markets are actually quite creative, and you have several vehicles to choose from. The reason there are so many different kinds is because every business is different, and there is so much money in these debt markets that market forces bring new products to life every day.

To help demystify the world of financing with debt, I want to touch on a handful of popular ecommerce debt instruments and explain a few reasons why each one may be right for your business.

I've broken these down as simply as I can -- and if you find this article valuable, let me know, and I can dig into more detail in a follow-up post.

Disclaimer: Debt can be a dangerous tool. This content is for informational purposes only.

The ABL is the old-school loan that is secured by your assets. In other words, the lender will give you money, and if you can't pay them back, they will take all of your stuff. Important to note: the amount of money they are willing to lend to you is a percentage of your assets, or what is called your ‘borrowing base.’

So let’s say you have $1MM of finished goods inventory in your warehouse. You could go to any of the ABL players and hopefully have them extend you a facility for around 50% of your asset value. Congratulations! You have a $500K asset backed debt facility to draw on.

In summary, ABL is usually a tough fit for startups growing very quickly and can be sneakily expensive. Additionally, secured loans can make for a pretty hairy outcome in a downside situation.

Venture debt is a bit more straightforward. Essentially, there exists a market of lenders who are willing to lend to you based on whether or not they think you will raise another equity round with a standard ‘Term Loan’.

A term loan is a classic principal + interest loan paid back over a specified duration of time. If you raise the next equity round, you can pay them back. If debt to equity capitalization is a spectrum of risk/reward, these lenders fall somewhere in the middle.

Fun fact: often you'll see funding announcements that are actually part equity, part venture debt. For instance, you might see a $20M Series B announcement. But behind the scenes, it was really $15M of Series B equity and $5M of venture debt. This helps the company get X more months of runway - without dilution - beyond the Series B issuance.

SBA loans are guaranteed by the government (via the Small Business Administration) and administered by banks for small businesses seeking capital. The most popular of these loans is known as the 7(a) loan program, which is a loan that has really flexible repayment terms as well as generally affordable interest rates.

Generally speaking, I would avoid these types of loans as a VC-backed founder as they come with personal guarantees (PGs), and if your business goes under, you are personally liable for the principal.

Pros:

Cons:

The MCA is my personal favorite for financing working capital of a hyper growth company. A merchant cash advance is a relatively new concept out of the last 5 years. Essentially, it is an open market receivables sale of your online business. What that means is you can sell your future revenue to any MCA supplier and they will advance you the amount of the receivables sale and charge you interest for putting the money in your pocket sooner.

MCA’s can get a bad rep, generally propagated by people who don’t fully understand them. It is true that these instruments can be ludicrously expensive when not negotiated properly. This is because they are paid back based on a remittance rate, or a percentage of your sales.

Therefore, if your sales begin to grow rapidly, you will pay back the loan + interest extremely quickly. If you end up paying off the whole loan +10% interest in 2 months because your business hit a huge growth spurt, you will have paid an effective 60% APR.

In my opinion, the reason this problem exists is because MCAs are so new that most lawyers don’t really understand them. Therefore, they are not able to effectively negotiate the terms of these deals, and unfortunately many founders end up paying ludicrous amounts in interest.

Good news: There is literally the easiest fix ever on this. You simply must negotiate remittance caps in order to achieve a desired APR. My last APR on an MCA was barely double digits, for a completely unsecured loan that I can draw on at any time. This is not always obvious to anyone who doesn't have familiarity modeling debt or IRRs, but it’s a fairly intuitive concept.

Pros:

Cons:

All in all, when it comes to financing, you have a lot of options to choose from -- especially on the debt side. It is important to understand all of the tools at your disposal so that you can ensure your business runs as smoothly as possible, properly finance operations, and avoid unnecessarily diluting your equity in the process.

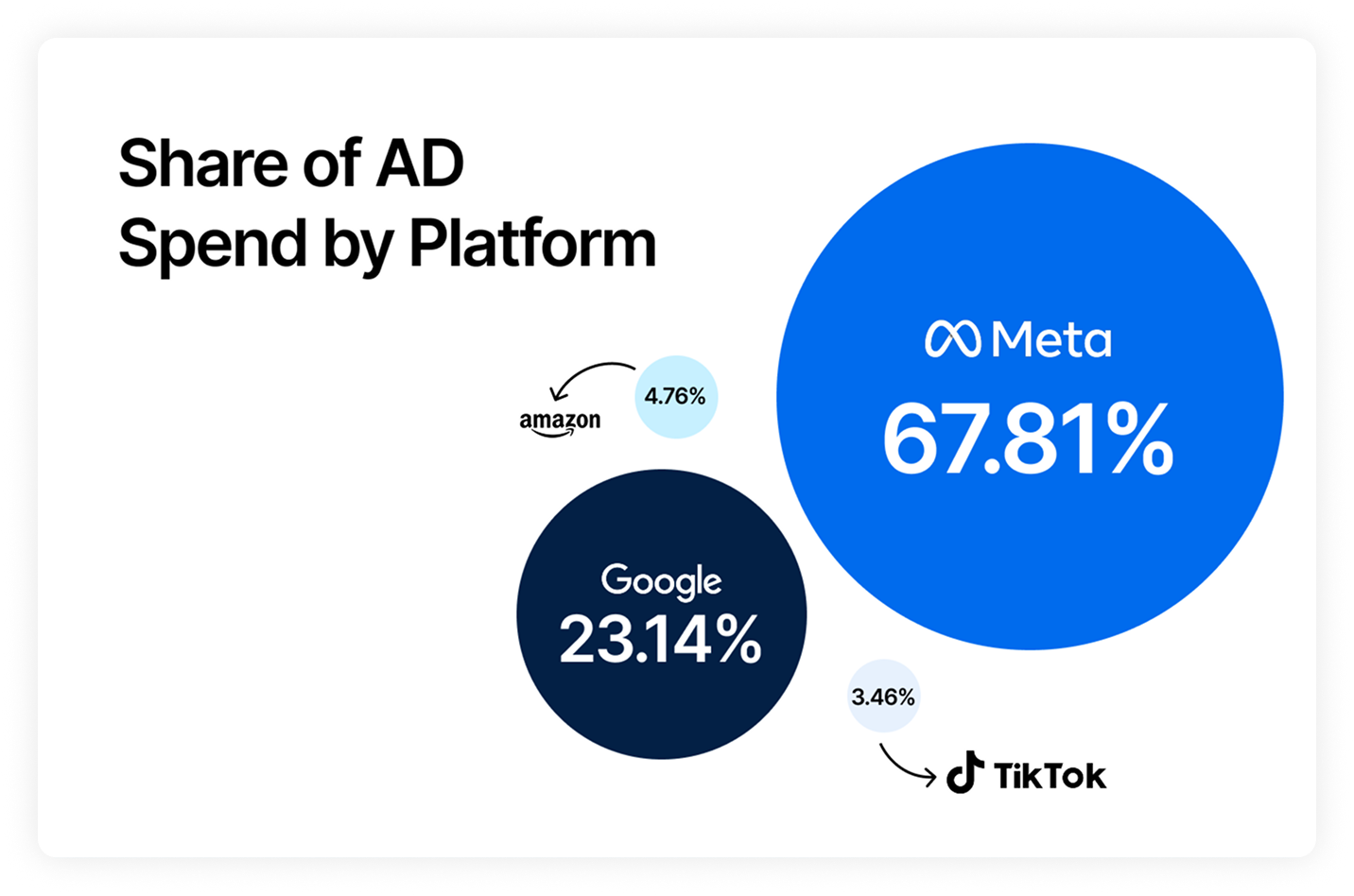

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)

.png)