There’s one thing that unifies all ecommerce marketers: staring at a dashboard and thinking, “Is this CPA actually good?”

The good news is, you’re not alone. It’s one of the most common questions in performance marketing. The bad news is, it’s a question that never really gets a straight answer.

Here’s why: a cost per acquisition (CPA) number on its own is meaningless. A $50 CPA could be incredible or catastrophic, depending on what you sell, how much you keep, and whether that customer ever comes back. CPA only makes sense when it’s tied to profitability.

This article breaks down what a good cost per acquisition actually looks like, gives you a practical framework to evaluate yours, and shows you how to set a target CPA that supports sustainable growth.

Key takeaways

A good cost per acquisition is one that allows you to acquire customers profitably, meaning the revenue a customer generates over their lifetime significantly exceeds what you paid to acquire them.

A widely used benchmark is an LTV:CPA ratio of around 3:1, which means for every $1 you spend acquiring a customer, they generate at least $3 in value. That said, there’s no single “good” CPA that applies to every business. What counts as good depends on your gross margins, business model, and the channel you’re acquiring through.

Think of it this way: CPA is an input. Profitability is the output. A $100 CPA is great if your customer lifetime value (LTV) is $500. That same $100 CPA is terrible if your LTV is $120. The number itself doesn’t tell you much. It’s the relationships between CPA and LTV that matters.

The most practical way to evaluate whether your CPA is good is through the LTV:CPA ratio. Technically, this is the LTV:CAC ratio, since customer acquisition cost (CAC) includes all acquisition spend, not just ad costs. But many ecommerce operators use CPA as a proxy for CAC, especially when paid media is their primary acquisition channel.

CPA varies dramatically across three dimensions:

Quick example: Two brands both have a $50 CPA. Brand A sells a $200 product with 65% gross margin. That’s $130 in gross profit, minus the $50 CPA, leaving $80 in contribution profit. Brand B sells an $80 product with 30% margin. That’s $24 in gross profit, minus $50 CPA, putting them $26 in the hole on every order. The same CPA, but opposite outcomes.

If CPA alone doesn’t tell you much, the LTV:CPA ratio fills in the gaps. It’s the single most useful metric for determining whether your acquisition costs are sustainable.

The LTV:CPA ratio compares how much a customer is worth over their entire relationship with your business (lifetime value) against how much it cost to acquire them. A 3:1 ratio means you earn $3 for every $1 you spend on acquisition.

For example: if your LTV is $300 and your CPA is $100, your LTV:CPA ratio is 3:1. If your LTV is $300 and your CPA is $200, your ratio drops 1.5:1, which signals a problem.

(Quick note on terminology: the “proper” version of this metric is LTV:CAC. But since many ecommerce brands use CPA and CAC interchangeably — especially when paid media is the primary customer acquisition cost driver — we’ll use CPA here.)

The 3:1 benchmark isn’t arbitrary. It exists because acquisition cost acquisition cost is only one piece of your cost structure. After you pay to acquire a customer, you still need to cover cost of goods sold, shipping and fulfillment, operating expenses (team, tools, rent), and leave enough to reinvest in growth.

At 3:1, roughly a third of a customer’s value goes toward acquisition, a third covers operations and COGS, and the remaining third is actual profit or investable margin. At 2:1 or below, there’s simply not enough room to run a sustainable business, especially in ecommerce, where margins are already tight.

That said, 3:1 is a starting point, not a ceiling. Subscription brands with strong retention might be profitable at 2.5:1 because they know customers stick around. High-margin luxury brands might need 4:1 because their operating costs are higher. The point is to use 3:1 as a gut-check baseline, then calibrate to your own unit economics.

Setting a target cost per acquisition starts with knowing your numbers — specifically, your customer lifetime value and your margins. Here’s how to work through it step by step:

Start by figuring what a customer is actually worth over time. The simplest way to calculate CLV is:

LTV = Average Order Value x Purchase Frequency x Customer Lifespan

Let’s say your AOV is $80, customers buy 3 times per year on average, and the typical customer stays active for 2 years. That gives you an LTV of $80 x 3 x 2 = $480.

LTV is a revenue number, not a profit number. You need to account for your gross margin to understand how much of that $480 is actually available to cover acquisition costs.

If your gross margin is 60%, your margin-adjusted LTV is $480 x 0.60 = $288.

Now divide your margin-adjusted LTV by your target ratio. Using the 3:1 benchmark:

Target CPA = $288 ÷ 3 = $96

That means you can afford to spend up to $96 to acquire a customer and still maintain a healthy return. If you want to be more conservative, target a 4:1 ratio and set your CPA ceiling at $72. If you’re in aggressive growth mode and can tolerate thinner margins, you might accept 2.5:1 and spend up to $115.

You can use the CPA formula (Total Marketing Spend ÷ Number of New Customers) to compare your actual CPA against this target and see where you stand.

One of the biggest mistakes in evaluating CPA is looking at the number in isolation. Two businesses can have the exact same CPA and end up in completely different financial positions. Here’s how:

Takeaway: The same CPA produces four completely different outcomes. Your AOV, margin, and LTV determine whether that CPA is a win or a red flag, not the number itself.

CPA benchmarks by industry provide a useful reference point, but should be considered in a directional context, not as targets. Your ideal CPA should come from your own unit economics. That said, knowing your industry benchmarks can help you spot red flags and calibrate expectations.

The following benchmarks are based on aggregated Triple Whale data from over 40,000 ecommerce ad accounts and $21 billion in ad spend over the trailing 12 months. These are median CPA figures. Industries with fewer than 100 ad accounts or under $1 million in total ad spend have been excluded.

Median CPAs across ecommerce industries range from roughly $26 to $50. The two largest categories by spend — Apparel & Accessories and Health & Beauty — both land right around $31, which makes that figure a reasonable baseline for DTC brands evaluating their own performance. Higher ticket verticals like Home & Garden, Electronics, and Travel Accessories & Luggage naturally sit higher in the $40-$43 range, while lower-AOV categories like Books, Baby, and Food & Beverage tend to cluster under $30.

It’s important again to note that these CPA benchmarks are medians, which can mask enormous variation within each industry. Use these numbers as a sanity check (and not as gospel).

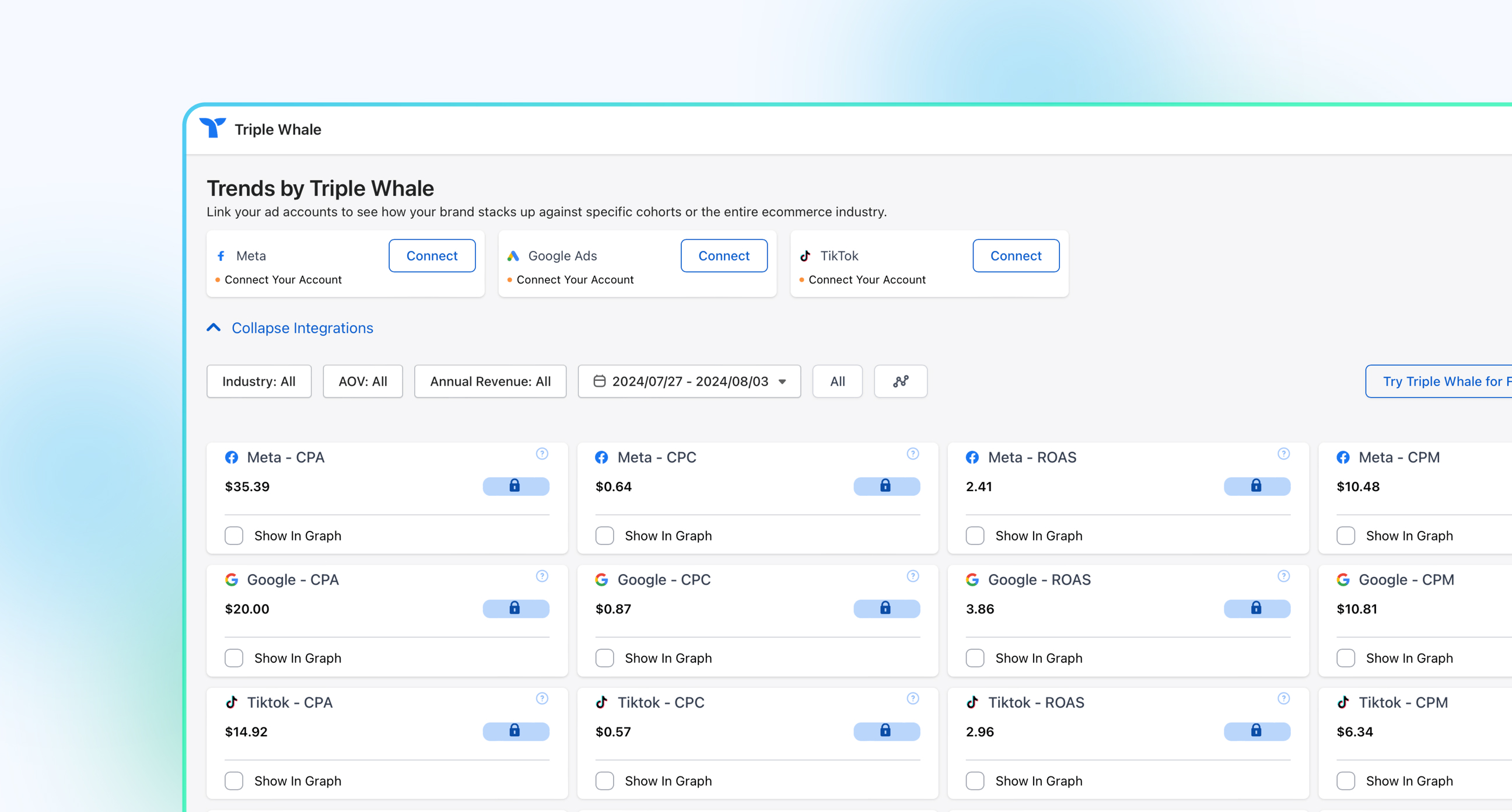

CPA will shift depending on which channel you’re using, and this data from over 42,000 Triple Whale brands (over the past 365 days) really breaks down which platforms are cheap on acquisition, and which are more pricey.

The key takeaway: you shouldn’t compare CPAs across channels and assume one is “better” or “best”. Each channel serves a different role in the funnel.

Here’s the thing about CPA: it’s only as accurate as the attribution model behind it.

If you’re using last-click attribution (which many platforms default to), your CPA is being assigned entirely to the last touchpoint before conversion. That means your Google brand search campaign might look incredibly efficient — while your prospecting campaigns on Meta look expensive — even though Meta is what introduced the customer in the first place.

Multi-touch attribution models distribute credit more evenly across the customer journey, which often shifts CPA significantly. A campaign that looked like it had $120 CPA under last-click might actually have a $60 CPA under a multi-touch model, because it’s now sharing credit with other touchpoints.

Why this matters for setting targets: If your CPA data is distorted by your attribution model, your targets will be off too. Before you decide your CPA is “too high” or “too low”, make sure you understand how credit is being assigned. It’s one of the biggest hidden factors in CPA evaluation.

Once you’ve set a target CPA and compared it against your actual numbers, you’ll fall into one of two camps. Here’s what to do in each scenario.

Pulling it all together, here’s the step-by-step process for setting a target cost per acquisition that’s grounded in your actual business:

There’s no magic number that makes a CPA “good”. The only CPA that matters is the one you can directly tie to profitability, which you only know when you understand your LTV, margins, and have a clear line of sight from acquisition cost to business performance.

Use the 3:1 LTV:CPA ratio as your baseline. Calibrate with your own AOV, margins, and repeat purchase data. Frame industry benchmarks as directional context, not gospel. And always question whether your attribution model is giving you the full picture.

Triple Whale gives ecommerce brands the ability to see CPA, LTV, AOV, and attribution data in one place, so you’re never making acquisition decisions based on only part of the story. If you’re tired of guessing whether your CPA is “good”, it might be time to get the full picture.

CPA benchmarks for ecommerce generally range from $10 to $100, but a “good” CPA depends on your AOV, gross margin, and customer lifetime value. The most reliable test: is your LTV:CPA ratio at least 3:1? If so, your CPA is likely sustainable.

Not necessarily. A very low CPA can signal that you’re only reaching easy-to-convert audiences and underinvesting in growth. The goal isn’t the lowest possible CPA, it’s the highest CPA you can sustain while still hitting your profitability targets.

A 3:1 ratio is widely considered the benchmark for healthy, sustainable growth. Below 2:1, you’re likely losing money after covering COGS and overhead. Above 5:1, you may be underinvesting in acquisition and missing scaling opportunities.

Attribution models determine how credit for conversions is assigned across touchpoints. Last-click attribution gives all the credit to the final click, which can make some channels look cheap and others look expensive. Multi-touch models spread credit more evenly, often revealing that your “expensive” prospecting channels are actually more efficient than last-click suggests.

CPA (cost per acquisition) typically refers to the cost of a specific conversion action — like a purchase or a lead — on a single channel. CAC (customer acquisition cost) is broader: it includes all marketing and sales spend divided by total new customers acquired. In practice, many ecommerce brands use CPA and CAC interchangeably, but they’re technically different.

There’s one thing that unifies all ecommerce marketers: staring at a dashboard and thinking, “Is this CPA actually good?”

The good news is, you’re not alone. It’s one of the most common questions in performance marketing. The bad news is, it’s a question that never really gets a straight answer.

Here’s why: a cost per acquisition (CPA) number on its own is meaningless. A $50 CPA could be incredible or catastrophic, depending on what you sell, how much you keep, and whether that customer ever comes back. CPA only makes sense when it’s tied to profitability.

This article breaks down what a good cost per acquisition actually looks like, gives you a practical framework to evaluate yours, and shows you how to set a target CPA that supports sustainable growth.

Key takeaways

A good cost per acquisition is one that allows you to acquire customers profitably, meaning the revenue a customer generates over their lifetime significantly exceeds what you paid to acquire them.

A widely used benchmark is an LTV:CPA ratio of around 3:1, which means for every $1 you spend acquiring a customer, they generate at least $3 in value. That said, there’s no single “good” CPA that applies to every business. What counts as good depends on your gross margins, business model, and the channel you’re acquiring through.

Think of it this way: CPA is an input. Profitability is the output. A $100 CPA is great if your customer lifetime value (LTV) is $500. That same $100 CPA is terrible if your LTV is $120. The number itself doesn’t tell you much. It’s the relationships between CPA and LTV that matters.

The most practical way to evaluate whether your CPA is good is through the LTV:CPA ratio. Technically, this is the LTV:CAC ratio, since customer acquisition cost (CAC) includes all acquisition spend, not just ad costs. But many ecommerce operators use CPA as a proxy for CAC, especially when paid media is their primary acquisition channel.

CPA varies dramatically across three dimensions:

Quick example: Two brands both have a $50 CPA. Brand A sells a $200 product with 65% gross margin. That’s $130 in gross profit, minus the $50 CPA, leaving $80 in contribution profit. Brand B sells an $80 product with 30% margin. That’s $24 in gross profit, minus $50 CPA, putting them $26 in the hole on every order. The same CPA, but opposite outcomes.

If CPA alone doesn’t tell you much, the LTV:CPA ratio fills in the gaps. It’s the single most useful metric for determining whether your acquisition costs are sustainable.

The LTV:CPA ratio compares how much a customer is worth over their entire relationship with your business (lifetime value) against how much it cost to acquire them. A 3:1 ratio means you earn $3 for every $1 you spend on acquisition.

For example: if your LTV is $300 and your CPA is $100, your LTV:CPA ratio is 3:1. If your LTV is $300 and your CPA is $200, your ratio drops 1.5:1, which signals a problem.

(Quick note on terminology: the “proper” version of this metric is LTV:CAC. But since many ecommerce brands use CPA and CAC interchangeably — especially when paid media is the primary customer acquisition cost driver — we’ll use CPA here.)

The 3:1 benchmark isn’t arbitrary. It exists because acquisition cost acquisition cost is only one piece of your cost structure. After you pay to acquire a customer, you still need to cover cost of goods sold, shipping and fulfillment, operating expenses (team, tools, rent), and leave enough to reinvest in growth.

At 3:1, roughly a third of a customer’s value goes toward acquisition, a third covers operations and COGS, and the remaining third is actual profit or investable margin. At 2:1 or below, there’s simply not enough room to run a sustainable business, especially in ecommerce, where margins are already tight.

That said, 3:1 is a starting point, not a ceiling. Subscription brands with strong retention might be profitable at 2.5:1 because they know customers stick around. High-margin luxury brands might need 4:1 because their operating costs are higher. The point is to use 3:1 as a gut-check baseline, then calibrate to your own unit economics.

Setting a target cost per acquisition starts with knowing your numbers — specifically, your customer lifetime value and your margins. Here’s how to work through it step by step:

Start by figuring what a customer is actually worth over time. The simplest way to calculate CLV is:

LTV = Average Order Value x Purchase Frequency x Customer Lifespan

Let’s say your AOV is $80, customers buy 3 times per year on average, and the typical customer stays active for 2 years. That gives you an LTV of $80 x 3 x 2 = $480.

LTV is a revenue number, not a profit number. You need to account for your gross margin to understand how much of that $480 is actually available to cover acquisition costs.

If your gross margin is 60%, your margin-adjusted LTV is $480 x 0.60 = $288.

Now divide your margin-adjusted LTV by your target ratio. Using the 3:1 benchmark:

Target CPA = $288 ÷ 3 = $96

That means you can afford to spend up to $96 to acquire a customer and still maintain a healthy return. If you want to be more conservative, target a 4:1 ratio and set your CPA ceiling at $72. If you’re in aggressive growth mode and can tolerate thinner margins, you might accept 2.5:1 and spend up to $115.

You can use the CPA formula (Total Marketing Spend ÷ Number of New Customers) to compare your actual CPA against this target and see where you stand.

One of the biggest mistakes in evaluating CPA is looking at the number in isolation. Two businesses can have the exact same CPA and end up in completely different financial positions. Here’s how:

Takeaway: The same CPA produces four completely different outcomes. Your AOV, margin, and LTV determine whether that CPA is a win or a red flag, not the number itself.

CPA benchmarks by industry provide a useful reference point, but should be considered in a directional context, not as targets. Your ideal CPA should come from your own unit economics. That said, knowing your industry benchmarks can help you spot red flags and calibrate expectations.

The following benchmarks are based on aggregated Triple Whale data from over 40,000 ecommerce ad accounts and $21 billion in ad spend over the trailing 12 months. These are median CPA figures. Industries with fewer than 100 ad accounts or under $1 million in total ad spend have been excluded.

Median CPAs across ecommerce industries range from roughly $26 to $50. The two largest categories by spend — Apparel & Accessories and Health & Beauty — both land right around $31, which makes that figure a reasonable baseline for DTC brands evaluating their own performance. Higher ticket verticals like Home & Garden, Electronics, and Travel Accessories & Luggage naturally sit higher in the $40-$43 range, while lower-AOV categories like Books, Baby, and Food & Beverage tend to cluster under $30.

It’s important again to note that these CPA benchmarks are medians, which can mask enormous variation within each industry. Use these numbers as a sanity check (and not as gospel).

CPA will shift depending on which channel you’re using, and this data from over 42,000 Triple Whale brands (over the past 365 days) really breaks down which platforms are cheap on acquisition, and which are more pricey.

The key takeaway: you shouldn’t compare CPAs across channels and assume one is “better” or “best”. Each channel serves a different role in the funnel.

Here’s the thing about CPA: it’s only as accurate as the attribution model behind it.

If you’re using last-click attribution (which many platforms default to), your CPA is being assigned entirely to the last touchpoint before conversion. That means your Google brand search campaign might look incredibly efficient — while your prospecting campaigns on Meta look expensive — even though Meta is what introduced the customer in the first place.

Multi-touch attribution models distribute credit more evenly across the customer journey, which often shifts CPA significantly. A campaign that looked like it had $120 CPA under last-click might actually have a $60 CPA under a multi-touch model, because it’s now sharing credit with other touchpoints.

Why this matters for setting targets: If your CPA data is distorted by your attribution model, your targets will be off too. Before you decide your CPA is “too high” or “too low”, make sure you understand how credit is being assigned. It’s one of the biggest hidden factors in CPA evaluation.

Once you’ve set a target CPA and compared it against your actual numbers, you’ll fall into one of two camps. Here’s what to do in each scenario.

Pulling it all together, here’s the step-by-step process for setting a target cost per acquisition that’s grounded in your actual business:

There’s no magic number that makes a CPA “good”. The only CPA that matters is the one you can directly tie to profitability, which you only know when you understand your LTV, margins, and have a clear line of sight from acquisition cost to business performance.

Use the 3:1 LTV:CPA ratio as your baseline. Calibrate with your own AOV, margins, and repeat purchase data. Frame industry benchmarks as directional context, not gospel. And always question whether your attribution model is giving you the full picture.

Triple Whale gives ecommerce brands the ability to see CPA, LTV, AOV, and attribution data in one place, so you’re never making acquisition decisions based on only part of the story. If you’re tired of guessing whether your CPA is “good”, it might be time to get the full picture.

CPA benchmarks for ecommerce generally range from $10 to $100, but a “good” CPA depends on your AOV, gross margin, and customer lifetime value. The most reliable test: is your LTV:CPA ratio at least 3:1? If so, your CPA is likely sustainable.

Not necessarily. A very low CPA can signal that you’re only reaching easy-to-convert audiences and underinvesting in growth. The goal isn’t the lowest possible CPA, it’s the highest CPA you can sustain while still hitting your profitability targets.

A 3:1 ratio is widely considered the benchmark for healthy, sustainable growth. Below 2:1, you’re likely losing money after covering COGS and overhead. Above 5:1, you may be underinvesting in acquisition and missing scaling opportunities.

Attribution models determine how credit for conversions is assigned across touchpoints. Last-click attribution gives all the credit to the final click, which can make some channels look cheap and others look expensive. Multi-touch models spread credit more evenly, often revealing that your “expensive” prospecting channels are actually more efficient than last-click suggests.

CPA (cost per acquisition) typically refers to the cost of a specific conversion action — like a purchase or a lead — on a single channel. CAC (customer acquisition cost) is broader: it includes all marketing and sales spend divided by total new customers acquired. In practice, many ecommerce brands use CPA and CAC interchangeably, but they’re technically different.

A good cost per acquisition depends on LTV and margins. Learn how to evaluate cost per acquisition using LTV ratios, AOV, and real benchmarks.

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)

.png)