The world of eCom can get pretty complicated sometimes. It seems like we’re involved in the only industry that requires mastery in marketing, supply chain and logistics, PR, analytics, and finance.

It’s a-lot to handle, especially when you have to juggle your bookkeeping and reconciliation at the end of the month.

We’re darned if we do and darned if we don’t, because regardless of how we feel about it, Uncle Sam is patiently waiting for his royalty check at the end of the year.

Luckily, the team at Triple Whale blessed us with FinHub, but even then, what even is accounting? And what does it mean for my business?

For starters, we have to take inventory (no pun intended) of how we want to account for our books and what it all really means.

Should I start on a cash basis or accrual basis— and what does that even mean?

What do my investors want to see?

What are my tax implications at the end of the year?

What if I'm selling wholesale?

What is the value of my inventory?

What sifts to my P/L, and what are the assets on my balance sheet?

You can hire a CPA for $500/hr to answer these questions with jargon that even they don’t understand, or you can read this short snippet from the lens of a DTC operator turned bookkeeping agency owner.

We’re going to answer all of your questions, make it easy to swallow, and equip you with ALL the info you need to succeed.

But before we do, we need to learn the fundamental difference between cash and accrual basis accounting. We’ll add the cherry on top at the end.

Cash basis accounting is a simple approach to business accounting and the perfect option if you’re just starting out (or before $1,000,000 in revenue). It records income and expenses as they’re received or paid, rather than as they’re earned or incurred.

This approach is especially useful for small businesses with limited cash flow, because it doesn't require any JE’s (journal entries) to be created.

Instead, the cash basis method simply matches expenses with their related revenue when payments are made (or received).

You also don’t need to worry about tracking the value of your inventory, account payables (money you owe to vendors), account receivables (money owed to you by customers) or bad debts, amortized or depreciating assets (whatever that means), and more.

Because JE’s aren’t required, cash basis accounting is an excellent choice for eCom stores transactions or whose operations are simple enough that they don't require complicated financial statements.

No need to manage COGS from wholesale/retail sales, or your accounts receivables in general. You’ll only recognize that revenue when it’s paid, not earned.

The perpetual inventory system is a record of all purchases and sales, as well as the quantity of each item on hand. This information is updated daily or periodically to keep track of inventory levels.

For example, if you buy 10 cases of wine and sell 5 cases, you do not need to update your inventory until you use up the remaining five cases or make another sale.

Cash basis accounting is easy to get started with, but can become inefficient for more complicated businesses.

Once you start taking on loans, selling to customers on net terms, purchasing inventory, and overall scale your business… I’d suggest you switch over to accrual.

As easy as it is to account for, cash basis accounting won’t offer the clarity and insight you need to make business decisions.

Sally buys $100 worth of hats, and each hat costs her $5. She posts it on her Shopify store-front for $10/hat and sells $50 worth (5 hats) in a month.

At the end of the month, her profit would be -$50.

Why?

On paper (or cash basis accounting), 100% of the she invested in inventory would be expensed on her P/L immediately, and since she only generates $50 in sales, her P/L would show at a loss. Regardless if her COGS (cost of goods sold) is technically only $25.

For small businesses that need to track their books and don’t want to complicate their day-to-day or pay to outsource their books to a professional.

Pros:

•It’s very simple to account for.

•You know exactly how much cash you have at any given time.

•It doesn’t require a bookkeeper or CPA to keep track of or outsource

Cons:

•It lacks the detail and insight of your day-to-day and future business operations

•You can outgrow cash basis accounting quickly

•Managing your inventory value will be difficult

•Account Payables & Account Receivables are not accounted for

Accrual basis accounting is used by most businesses as their preferred accounting method. It involves recording transactions when they occur, regardless of when cash changes hands.

Accrual accounting can help businesses forecast their future cash flow needs more accurately and make better decisions about borrowing money or issuing stock.

In accrual accounting, transactions are recorded when they occur, regardless of when cash changes hands.

Accrual accounting is different from cash accounting because it records revenue when you earn it, regardless of whether or not you've been paid yet.

The idea behind accrual accounting is that by recording sales upfront, businesses can be more accurate in their projections and have better control over their finances.

In financial statements, this means a company's assets and liabilities will be higher than what they actually have on hand at any given moment—because you’ll often sell your product before receiving payment!

In other words, when you look at a company's balance sheet (which shows its assets), there's always going to be more than what's listed as "cash."

Account payables and account receivables are both treated as current liabilities and assets respectively.

Accounts payable is defined as any money owed by a business to its suppliers for goods purchased on credit within the last 12 months. In other words, this is money you owe.

Accounts receivable are defined as funds that are owed to a business from customers that have purchased goods within the last 12 months. In other words, this is money you’re owed.

Account Payables = Money Going Out

Account Receivables = Money Coming In

Accrued revenue is the same thing as accounts receivable, which is an asset. The company has earned the revenue, but it hasn't yet been paid for by its customer.

This unpaid revenue is recorded on the balance sheet as an account receivable. The business will eventually collect this money from its customers, so it's called "accrued" because it hasn't yet been paid for.

Unlike cash basis, accrual accounting needs to track your inventory purchases and assets in detail.

Instead of deducting it on your P/L under COGS, it’s sifted to your inventory assets COA (chart of account) on your balance sheet as an asset.

As your products sell, you’ll need to:

This technique offers a much more accurate tell of what inventory (or raw materials) you have on hand, how much product you’ve sold over any given period of time, and what your true profitability is.

It is, on the other hand, more labor intensive to account for.

In this same example, Sally buys $100 worth of hats, and each hat cost her $5. She posts it on her Shopify store-front for $10/hat and sells $50 worth (5 hats) in a month.

At the end of the month, her profit would be $25.00

Woah… that’s a $75 difference (from -$50 to +$25)

Why?

The $100 she spent on inventory would sift into her Balance Sheet as an ASSET. It would NOT be expensed on her P/L under COGS. Only the units sold that month will be.

Since she sold 5 units (at $5 per unit), her COGS equates to $25.00. That sifts into her COGS.

Her revenue generated was $50.

$50 - $25 = $25 in profit.

For any business that’s scaling and requires a true account for the health of their business.

Pros:

•Delivers an accurate picture of the performance of your business

•Preferred by investors

•Aligns with GAAP standards

•Accounts for Inventory, Account Payables and Account Receivables

Cons:

•Cash flow projections are required to understand the true performance of your business

•Requires a professional CPA or bookkeeper to manage

•More complicated with higher risk of error when accounting for

Whether you’re thinking of starting with a cash basis or accrual basis, the honest answer is: It really depends on your use case.

If you’re just starting out, cash basis accounting is a great choice. It’s simple and easy to understand, so it won’t take much time to get started. And since you don’t have to worry about adjusting for changes in inventory or depreciation, you can focus on growing your business without worrying about keeping track of complicated finances.

However, as your company grows in size and complexity (and this happens quickly!), cash basis accounting may not be the best option anymore and it might be time to switch over to accrual.

We hope that you now have a better understanding of accrual accounting and why it is used in larger businesses. Accrual-based accounting provides more information about your company's performance over time, which is why it has become the standard for reporting financial results

The world of eCom can get pretty complicated sometimes. It seems like we’re involved in the only industry that requires mastery in marketing, supply chain and logistics, PR, analytics, and finance.

It’s a-lot to handle, especially when you have to juggle your bookkeeping and reconciliation at the end of the month.

We’re darned if we do and darned if we don’t, because regardless of how we feel about it, Uncle Sam is patiently waiting for his royalty check at the end of the year.

Luckily, the team at Triple Whale blessed us with FinHub, but even then, what even is accounting? And what does it mean for my business?

For starters, we have to take inventory (no pun intended) of how we want to account for our books and what it all really means.

Should I start on a cash basis or accrual basis— and what does that even mean?

What do my investors want to see?

What are my tax implications at the end of the year?

What if I'm selling wholesale?

What is the value of my inventory?

What sifts to my P/L, and what are the assets on my balance sheet?

You can hire a CPA for $500/hr to answer these questions with jargon that even they don’t understand, or you can read this short snippet from the lens of a DTC operator turned bookkeeping agency owner.

We’re going to answer all of your questions, make it easy to swallow, and equip you with ALL the info you need to succeed.

But before we do, we need to learn the fundamental difference between cash and accrual basis accounting. We’ll add the cherry on top at the end.

Cash basis accounting is a simple approach to business accounting and the perfect option if you’re just starting out (or before $1,000,000 in revenue). It records income and expenses as they’re received or paid, rather than as they’re earned or incurred.

This approach is especially useful for small businesses with limited cash flow, because it doesn't require any JE’s (journal entries) to be created.

Instead, the cash basis method simply matches expenses with their related revenue when payments are made (or received).

You also don’t need to worry about tracking the value of your inventory, account payables (money you owe to vendors), account receivables (money owed to you by customers) or bad debts, amortized or depreciating assets (whatever that means), and more.

Because JE’s aren’t required, cash basis accounting is an excellent choice for eCom stores transactions or whose operations are simple enough that they don't require complicated financial statements.

No need to manage COGS from wholesale/retail sales, or your accounts receivables in general. You’ll only recognize that revenue when it’s paid, not earned.

The perpetual inventory system is a record of all purchases and sales, as well as the quantity of each item on hand. This information is updated daily or periodically to keep track of inventory levels.

For example, if you buy 10 cases of wine and sell 5 cases, you do not need to update your inventory until you use up the remaining five cases or make another sale.

Cash basis accounting is easy to get started with, but can become inefficient for more complicated businesses.

Once you start taking on loans, selling to customers on net terms, purchasing inventory, and overall scale your business… I’d suggest you switch over to accrual.

As easy as it is to account for, cash basis accounting won’t offer the clarity and insight you need to make business decisions.

Sally buys $100 worth of hats, and each hat costs her $5. She posts it on her Shopify store-front for $10/hat and sells $50 worth (5 hats) in a month.

At the end of the month, her profit would be -$50.

Why?

On paper (or cash basis accounting), 100% of the she invested in inventory would be expensed on her P/L immediately, and since she only generates $50 in sales, her P/L would show at a loss. Regardless if her COGS (cost of goods sold) is technically only $25.

For small businesses that need to track their books and don’t want to complicate their day-to-day or pay to outsource their books to a professional.

Pros:

•It’s very simple to account for.

•You know exactly how much cash you have at any given time.

•It doesn’t require a bookkeeper or CPA to keep track of or outsource

Cons:

•It lacks the detail and insight of your day-to-day and future business operations

•You can outgrow cash basis accounting quickly

•Managing your inventory value will be difficult

•Account Payables & Account Receivables are not accounted for

Accrual basis accounting is used by most businesses as their preferred accounting method. It involves recording transactions when they occur, regardless of when cash changes hands.

Accrual accounting can help businesses forecast their future cash flow needs more accurately and make better decisions about borrowing money or issuing stock.

In accrual accounting, transactions are recorded when they occur, regardless of when cash changes hands.

Accrual accounting is different from cash accounting because it records revenue when you earn it, regardless of whether or not you've been paid yet.

The idea behind accrual accounting is that by recording sales upfront, businesses can be more accurate in their projections and have better control over their finances.

In financial statements, this means a company's assets and liabilities will be higher than what they actually have on hand at any given moment—because you’ll often sell your product before receiving payment!

In other words, when you look at a company's balance sheet (which shows its assets), there's always going to be more than what's listed as "cash."

Account payables and account receivables are both treated as current liabilities and assets respectively.

Accounts payable is defined as any money owed by a business to its suppliers for goods purchased on credit within the last 12 months. In other words, this is money you owe.

Accounts receivable are defined as funds that are owed to a business from customers that have purchased goods within the last 12 months. In other words, this is money you’re owed.

Account Payables = Money Going Out

Account Receivables = Money Coming In

Accrued revenue is the same thing as accounts receivable, which is an asset. The company has earned the revenue, but it hasn't yet been paid for by its customer.

This unpaid revenue is recorded on the balance sheet as an account receivable. The business will eventually collect this money from its customers, so it's called "accrued" because it hasn't yet been paid for.

Unlike cash basis, accrual accounting needs to track your inventory purchases and assets in detail.

Instead of deducting it on your P/L under COGS, it’s sifted to your inventory assets COA (chart of account) on your balance sheet as an asset.

As your products sell, you’ll need to:

This technique offers a much more accurate tell of what inventory (or raw materials) you have on hand, how much product you’ve sold over any given period of time, and what your true profitability is.

It is, on the other hand, more labor intensive to account for.

In this same example, Sally buys $100 worth of hats, and each hat cost her $5. She posts it on her Shopify store-front for $10/hat and sells $50 worth (5 hats) in a month.

At the end of the month, her profit would be $25.00

Woah… that’s a $75 difference (from -$50 to +$25)

Why?

The $100 she spent on inventory would sift into her Balance Sheet as an ASSET. It would NOT be expensed on her P/L under COGS. Only the units sold that month will be.

Since she sold 5 units (at $5 per unit), her COGS equates to $25.00. That sifts into her COGS.

Her revenue generated was $50.

$50 - $25 = $25 in profit.

For any business that’s scaling and requires a true account for the health of their business.

Pros:

•Delivers an accurate picture of the performance of your business

•Preferred by investors

•Aligns with GAAP standards

•Accounts for Inventory, Account Payables and Account Receivables

Cons:

•Cash flow projections are required to understand the true performance of your business

•Requires a professional CPA or bookkeeper to manage

•More complicated with higher risk of error when accounting for

Whether you’re thinking of starting with a cash basis or accrual basis, the honest answer is: It really depends on your use case.

If you’re just starting out, cash basis accounting is a great choice. It’s simple and easy to understand, so it won’t take much time to get started. And since you don’t have to worry about adjusting for changes in inventory or depreciation, you can focus on growing your business without worrying about keeping track of complicated finances.

However, as your company grows in size and complexity (and this happens quickly!), cash basis accounting may not be the best option anymore and it might be time to switch over to accrual.

We hope that you now have a better understanding of accrual accounting and why it is used in larger businesses. Accrual-based accounting provides more information about your company's performance over time, which is why it has become the standard for reporting financial results

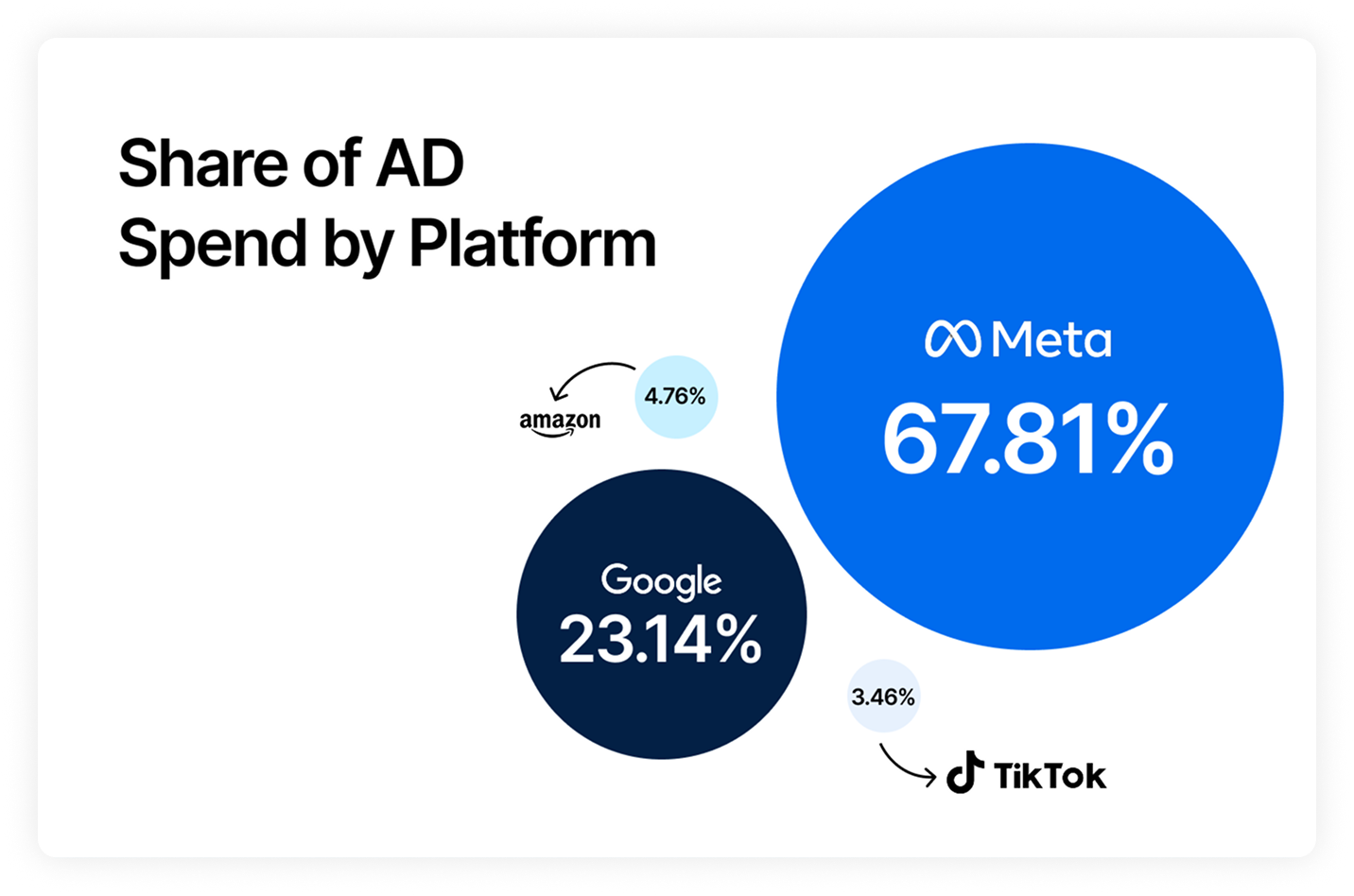

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)

.png)