Facebook remains the most popular platform for digital advertising on social media today, and its ad engine has become increasingly sophisticated over time. It not only has access to billions of people worldwide but also collects information about users, both online and offline, to create better ad targeting options for businesses.

In this article, we’ll outline some benefits of advertising on Facebook during this highly competitive period, including a closer look at some key statistics for how Triple Whale customers used Facebook ads during BFCM 2024.

Additionally, we’ll provide some ad examples and strategies for success when advertising on Facebook for BFCM 2025.

The number one reason for advertising on Facebook: it’s where the people are.

With more than three billion monthly active users, there’s a very large chance you’ll be able to connect with your target demographic when advertising on such a popular platform. In addition to its customer base, Facebook also offers unparalleled targeting capabilities, diverse ad formats, and audiences that are motivated to purchase products.

Here are some reasons why Facebook ads are particularly effective for BFCM campaigns:

These factors, combined with Facebook’s robust ad placement options and integration with other sales channels, make it one of the best platforms for maximizing BFCM traffic and sales.

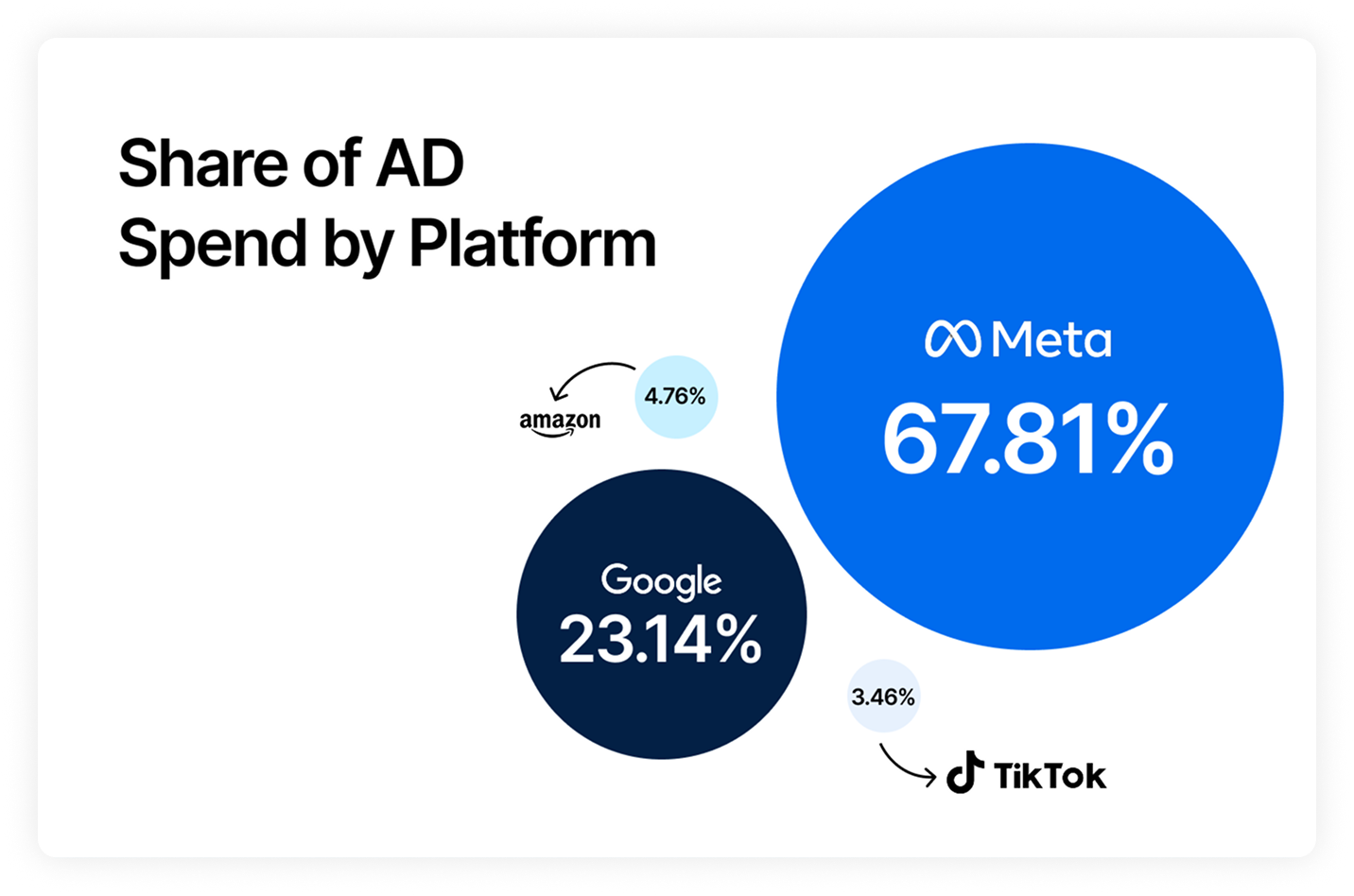

In our BFCM 2024 Retrospective Report, we evaluated the ad performance data for over 33,000 shops, comprising over $2 billion in revenue. There are some key statistics from the report that indicate Facebook/Meta remains a hot place to advertise for BFCM:

The less positive news:

To win BFCM in 2025, brands need to take a look back at their performance in 2024 to make confident, data-backed decisions to take their performance to the next level.

Meta is such a dominant platform, and the tried and true methods like carousel ads and Advantage+ campaigns are still in play, but to maximize ROI for BFCM 2025, here are some more strategies to consider:

One of the toughest parts of marketing is making sure your creative is fresh, lands with consumers, and is capitalizing on the latest trends in advertising. You could scour the Meta Ads Library to individually search for ads from brands you admire to emulate their approach, which could take hours of manual labour.

Or, you could have an AI agent do it all for you.

The Creative Inspiration Agent helps to accelerate high-converting creative production by analyzing successful ad campaigns and competitor strategies.

It can pull ads from the Meta Ads Library from the brands that inspire you, and analyze all of the elements that make the ad successful, from the hook, to the angles, USPs, and visual components.

Then, the agent will translate those successful patterns to fit your specific product, audience, and brand voice to generate a detailed brief with visual direction, scripts, and technical specifications so your team can be ready for immediate production of new content.

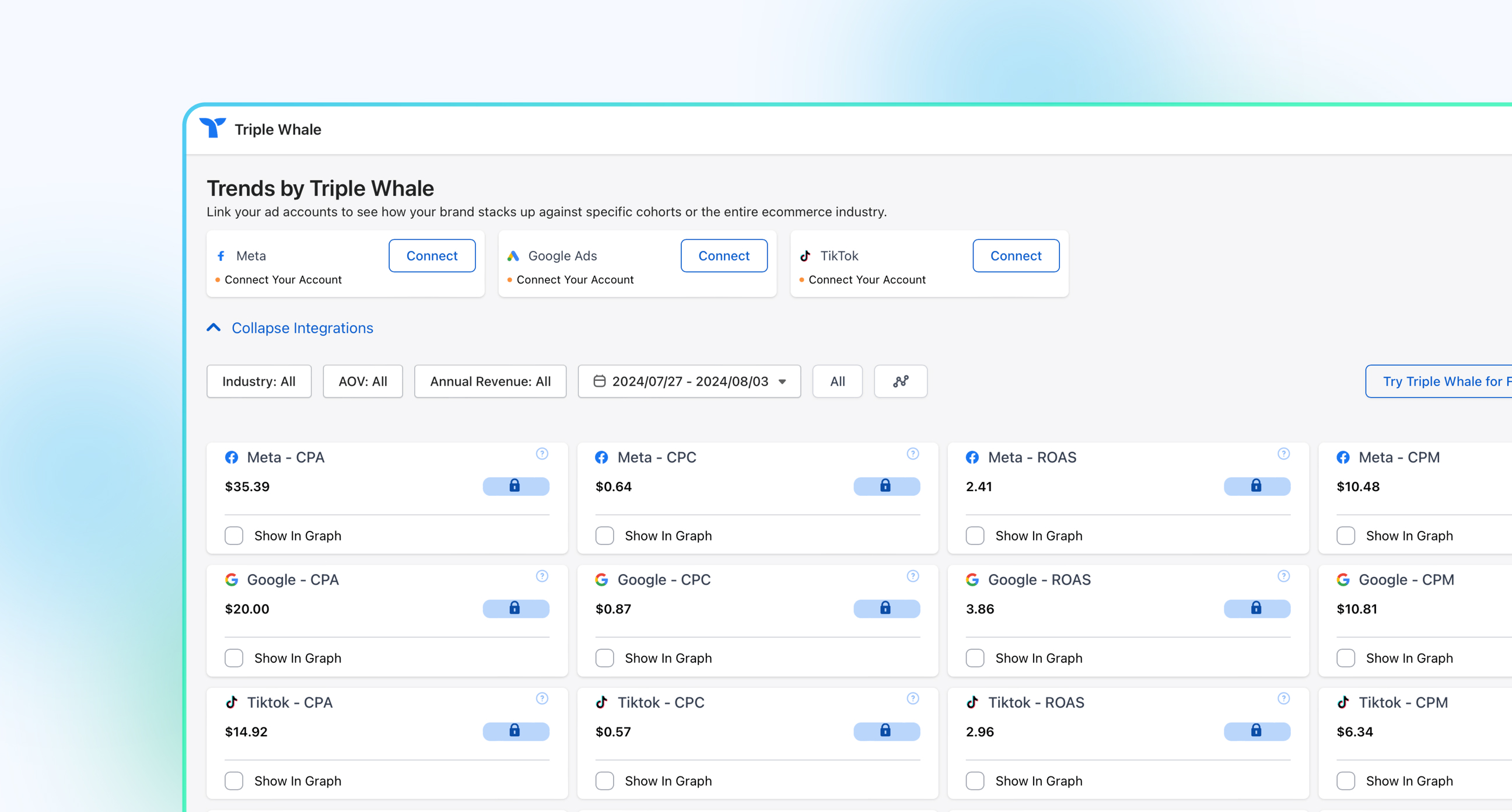

The Meta Ad Performance Agent can help optimize your Meta campaigns by analyzing key performance indicators (KPIs) like spend, CTR, and ROAS to identify trends in the ads you’re running.

It can identify which ads are driving the best results, what content is resonating with your audience to drive CTR, and help you make informed decisions to enhance your advertising strategy. By implementing this agent during BFCM, it will be easier to automatically spot which ads aren’t performing well, and to push ad spend to the high performers instead. This Agent will provide clear, actionable insights to simplify decision-making during a high-stress period.

The Meta Channel Performance Agent drives profitable growth by providing comprehensive, real-time analysis of Meta advertising across all campaign levels, including campaigns, ad sets, and individual ads. With period-over-period comparisons, it’s easier to see the performance changes with percentage metrics, and visual creative performance insights will have interactive media previews of top-performing ads.

With this Agent, brands can identify the top and underperforming campaigns and get immediate optimization and budget reallocation recommendations, with data-driven insights to drive better return on ad spend during BFCM.

Facebook continues to be a dominant platform for BFCM advertising, offering unparalleled targeting capabilities, diverse ad formats, and engaged audiences. With advanced targeting and retargeting options, dynamic ad formats, and robust data-driven insights, Facebook is an indispensable tool for brands aiming to maximize their reach and conversions during this peak shopping period.

Brands should take note of the ad performance trends outlined in this article to benchmark their BFCM 2024 data and prepare for 2025, in addition to employing some AI-powered tools to optimize performance in real-time. Brands that combine these tactics with cross-channel coordination will be best positioned to capitalize on the biggest shopping period of the year.

Want to learn more about crushing BFCM 2025? Check out our BFCM Resource Hub to set yourself up for success!

Facebook remains the most popular platform for digital advertising on social media today, and its ad engine has become increasingly sophisticated over time. It not only has access to billions of people worldwide but also collects information about users, both online and offline, to create better ad targeting options for businesses.

In this article, we’ll outline some benefits of advertising on Facebook during this highly competitive period, including a closer look at some key statistics for how Triple Whale customers used Facebook ads during BFCM 2024.

Additionally, we’ll provide some ad examples and strategies for success when advertising on Facebook for BFCM 2025.

The number one reason for advertising on Facebook: it’s where the people are.

With more than three billion monthly active users, there’s a very large chance you’ll be able to connect with your target demographic when advertising on such a popular platform. In addition to its customer base, Facebook also offers unparalleled targeting capabilities, diverse ad formats, and audiences that are motivated to purchase products.

Here are some reasons why Facebook ads are particularly effective for BFCM campaigns:

These factors, combined with Facebook’s robust ad placement options and integration with other sales channels, make it one of the best platforms for maximizing BFCM traffic and sales.

In our BFCM 2024 Retrospective Report, we evaluated the ad performance data for over 33,000 shops, comprising over $2 billion in revenue. There are some key statistics from the report that indicate Facebook/Meta remains a hot place to advertise for BFCM:

The less positive news:

To win BFCM in 2025, brands need to take a look back at their performance in 2024 to make confident, data-backed decisions to take their performance to the next level.

Meta is such a dominant platform, and the tried and true methods like carousel ads and Advantage+ campaigns are still in play, but to maximize ROI for BFCM 2025, here are some more strategies to consider:

One of the toughest parts of marketing is making sure your creative is fresh, lands with consumers, and is capitalizing on the latest trends in advertising. You could scour the Meta Ads Library to individually search for ads from brands you admire to emulate their approach, which could take hours of manual labour.

Or, you could have an AI agent do it all for you.

The Creative Inspiration Agent helps to accelerate high-converting creative production by analyzing successful ad campaigns and competitor strategies.

It can pull ads from the Meta Ads Library from the brands that inspire you, and analyze all of the elements that make the ad successful, from the hook, to the angles, USPs, and visual components.

Then, the agent will translate those successful patterns to fit your specific product, audience, and brand voice to generate a detailed brief with visual direction, scripts, and technical specifications so your team can be ready for immediate production of new content.

The Meta Ad Performance Agent can help optimize your Meta campaigns by analyzing key performance indicators (KPIs) like spend, CTR, and ROAS to identify trends in the ads you’re running.

It can identify which ads are driving the best results, what content is resonating with your audience to drive CTR, and help you make informed decisions to enhance your advertising strategy. By implementing this agent during BFCM, it will be easier to automatically spot which ads aren’t performing well, and to push ad spend to the high performers instead. This Agent will provide clear, actionable insights to simplify decision-making during a high-stress period.

The Meta Channel Performance Agent drives profitable growth by providing comprehensive, real-time analysis of Meta advertising across all campaign levels, including campaigns, ad sets, and individual ads. With period-over-period comparisons, it’s easier to see the performance changes with percentage metrics, and visual creative performance insights will have interactive media previews of top-performing ads.

With this Agent, brands can identify the top and underperforming campaigns and get immediate optimization and budget reallocation recommendations, with data-driven insights to drive better return on ad spend during BFCM.

Facebook continues to be a dominant platform for BFCM advertising, offering unparalleled targeting capabilities, diverse ad formats, and engaged audiences. With advanced targeting and retargeting options, dynamic ad formats, and robust data-driven insights, Facebook is an indispensable tool for brands aiming to maximize their reach and conversions during this peak shopping period.

Brands should take note of the ad performance trends outlined in this article to benchmark their BFCM 2024 data and prepare for 2025, in addition to employing some AI-powered tools to optimize performance in real-time. Brands that combine these tactics with cross-channel coordination will be best positioned to capitalize on the biggest shopping period of the year.

Want to learn more about crushing BFCM 2025? Check out our BFCM Resource Hub to set yourself up for success!

Body Copy: The following benchmarks compare advertising metrics from April 1-17 to the previous period. Considering President Trump first unveiled his tariffs on April 2, the timing corresponds with potential changes in advertising behavior among ecommerce brands (though it isn’t necessarily correlated).

.webp)

.webp)

.png)

.png)

.png)

.png)